Summary

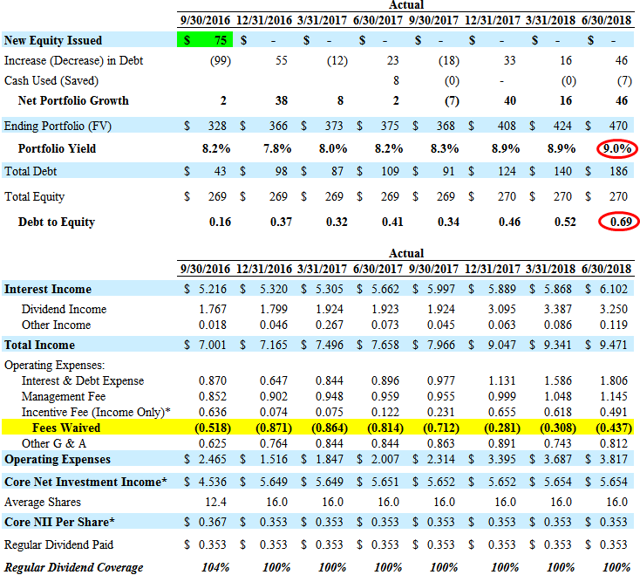

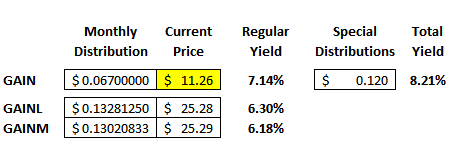

- For the quarter ended June 30, 2018, SUNS hit my base case projections covering its dividend thanks to continued fee waivers which have increased over the last two quarters.

- The Board approved a reduction in the minimum asset coverage ratio to 150% effective as of August 2, 2019, unless approved earlier by shareholders at its 2018 Annual Meeting.

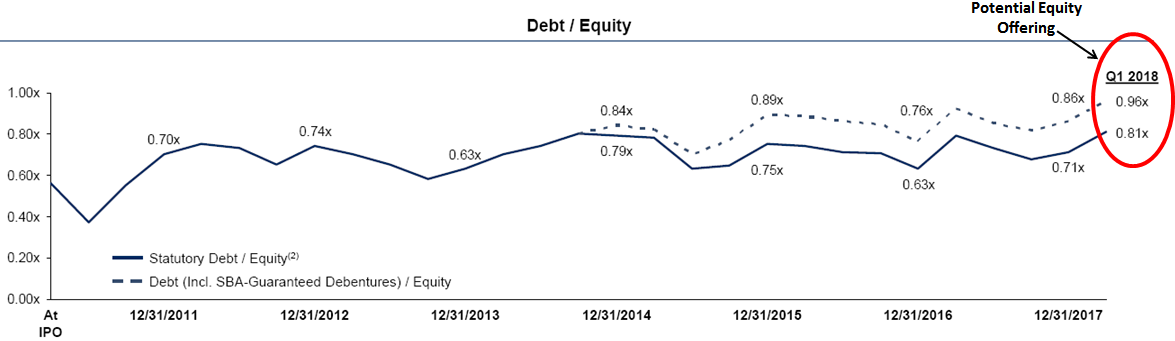

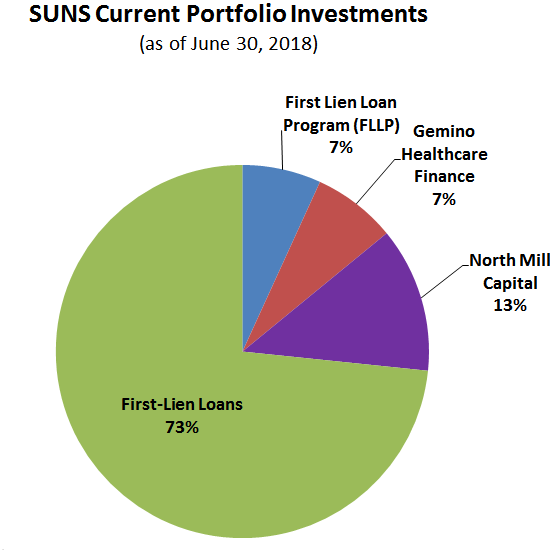

- NAV remained stable, portfolio growth was higher-than-expected increasing leverage to 0.69 and portfolio yield increased mostly due to North Mill Capital.

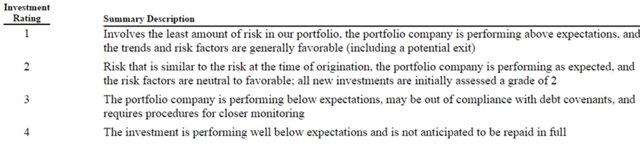

- Its first-lien investment in PPT Management Holdings, was added to non-accrual status with a cost of $7.8 million and fair value of $7.1 million (1.5% of the portfolio FV).

The following is a quick update that was previously provided to subscribers of Premium Reports on August 6, 2018. For target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs (including this one) please see Deep Dive Reports.

For the quarter ended June 30, 2018, Solar Senior Capital (SUNS) hit my base case projections covering its dividend thanks to continued fee waivers which increased from $0.308 million to $0.437 million as shown in the following table. The portfolio yield increased mostly due to North Mill Capital (“NMC”) that now accounts for 13% of the total portfolio and its weighted average yield increased from 12.9% to 13.3%. Portfolio growth was higher-than-expected and its debt-to-equity increased to 0.69 mostly due to new investments in its first-lien portion of the portfolio.

“We are pleased with Solar Senior Capital’s portfolio growth and operating performance in Q2 2018. Overall, the financial health of our portfolio companies remains sound,” said Michael Gross, Chairman and CEO of Solar Senior Capital Ltd. “Solar Senior’s comprehensive portfolio is predominantly comprised of first lien senior secured loans with floating rate coupons. We believe the Company is well positioned for the current environment and has the sourcing engines across cash flow and asset-based lending niches to drive additional portfolio growth and generate increased investment income.”

On August 2, 2018, the Board approved a reduction in the minimum asset coverage ratio from 200% to 150% effective as of August 2, 2019, unless approved earlier by the shareholders at its 2018 Annual Meeting. On June 1, 2018, its revolving credit facility was refinanced by way of amendment, allowing for an asset coverage ratio of 150%. On July 13, 2018, the credit facility was expanded by $25 million to $225 million. The company will target a range of 1.25x to 1.50x debt-to-equity, operating at a substantial cushion to the regulatory limit. Once the 150% coverage ratio becomes effective, the Company expects to use a modest amount of incremental leverage to continue to invest in its current mix of investments, including senior secured first lien cash flow and senior secured first lien specialty finance asset-based loans.

“Solar Senior Capital’s investment strategy is conducive to operating under the modified asset coverage ratio,” said Michael Gross, Chairman and CEO of Solar Senior Capital. “We believe that the senior secured first lien middle market loan asset class—Solar Senior Capital’s investment focus since inception—can prudently be levered above the previous BDC limits. We view this change as a significant opportunity to generate a greater return on equity for Solar Senior Capital.”

“The increased leverage flexibility will enable us to grow our senior secured first lien asset-based lending businesses and build and/or acquire other commercial finance platforms. We will finance the First Lien Loan Program’s loans directly on balance sheet, which will increase efficiencies and create new investment capacity for non-qualifying assets that, among other things, enables us to expand our specialty finance verticals,” said Bruce Spohler, Chief Operating Officer of Solar Senior Capital. “In summary, the asset coverage modification will enable us to do more of what we’ve been doing: investing in first lien, senior secured cash flow and asset-based loans.”

Its first-lien investment in PPT Management Holdings, LLC was added to non-accrual status during the quarter with a cost of $7.8 million and fair value of $7.1 million (1.5% of the portfolio FV). During the previous quarter, its first-lien investment in Metamorph US 3, LLC was added to non-accrual but was recently exited and responsible for most of the realized losses. However, its net asset value (“NAV”) per share has remained stable over the last two quarters due to markups including North Mill Capital and Gemino. The exit of Metamorph resulted in a decrease of investments with ‘rating 4’ as shown below:

As mentioned in previous reports, there is the potential for an upgrade as the company integrates and grows its recent acquisition/investment in North Mill Capital (“NMC”) as well as ramping its Solar Life Science Program LLC(“LSJV”) and First Lien Loan Program (“FLLP”) providing continued higher returns and overall portfolio yield growth. However, the company remains reliant on fee waivers to cover its dividend and as of June 30, 2018, the LSJV has not commenced operations.

NorthMill LLC

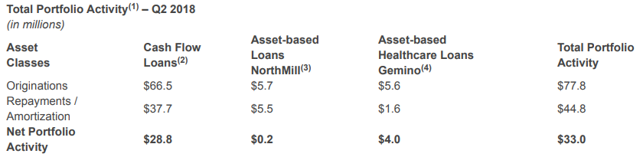

NorthMill currently manages a highly diverse portfolio of directly-originated and underwritten senior-secured commitments. As of June 30, 2018, the portfolio totaled approximately $322,813 of commitments, of which $162,983 were funded, on total assets of $188,189. At June 30, 2018, the portfolio consisted of 91 issuers with an average balance of approximately $1,791 versus 92 issuers with an average balance of approximately $1,600 at December 31, 2017. NMC has a senior credit facility with a bank lending group for $160,000 which expires on October 20, 2020. Borrowings are secured by substantially all of NMC’s assets. For the three months ended June 30, 2018, NMC had net income of $591 on gross income of $5,361. For the six months ended June 30, 2018, NMC had net income of $1,531 on gross income of $10,253.

Solar Life Science Lending

On February 22, 2017, Solar Senior Capital and its affiliates announced the formation of the Solar Life Science Program LLC (“LSJV”). LSJV is expected to invest the majority of its assets in first lien loans to publicly-traded companies in the U.S. life science industry. Solar Senior Capital has committed $75 million of equity to the joint venture. The joint venture has established a pipeline of investment opportunities to effectuate the ramping of LSJV’s investment portfolio. As of June 30, 2018, LSJV has not commenced operations.

Gemino Healthcare Finance LLC

As of June 30, 2018, the portfolio totaled approximately $173,588 of commitments, of which $111,334 were funded, on total assets of $106,357. At June 30, 2018, the portfolio consisted of 29 issuers with an average balance of approximately $3,839 versus 29 issuers with an average balance of approximately $3,677 at December 31, 2017. All of the commitments in Gemino’s portfolio are floating-rate, senior-secured, cash-pay loans. Gemino’s credit facility, which is non-recourse to us, had approximately $73,000 and $75,000 of borrowings outstanding at June 30, 2018 and December 31, 2017, respectively. For the three months ended June 30, 2018 and 2017, Gemino had net income of $668 and $655, respectively, on gross income of $2,745 and $2,760, respectively. For the six months ended June 30, 2018 and 2017, Gemino had net income of $1,380 and $1,423, respectively, on gross income of $5,464 and $5,611, respectively.

First Lien Loan Program LLC

As of June 30, 2018 and December 31, 2017, FLLP had total assets of $106,312 and $121,791, respectively. For the same periods, FLLP’s portfolio consisted of first lien floating rate senior secured loans to 19 and 23 different borrowers, respectively. For the three months ended June 30, 2018, FLLP invested $2,685 across 3 portfolio companies. For the three months ended June 30, 2017, FLLP invested $3,744 across 6 portfolio companies. Investments sold or prepaid totaled $19,870 for the three months ended June 30, 2018 and $8,626 for the three months ended June 30, 2017. At June 30, 2018 and December 31, 2017, the weighted average yield of FLLP’s portfolio was 7.4% and 7.3%, respectively, measured at fair value and 7.5% and 7.2%, respectively, measured at cost.

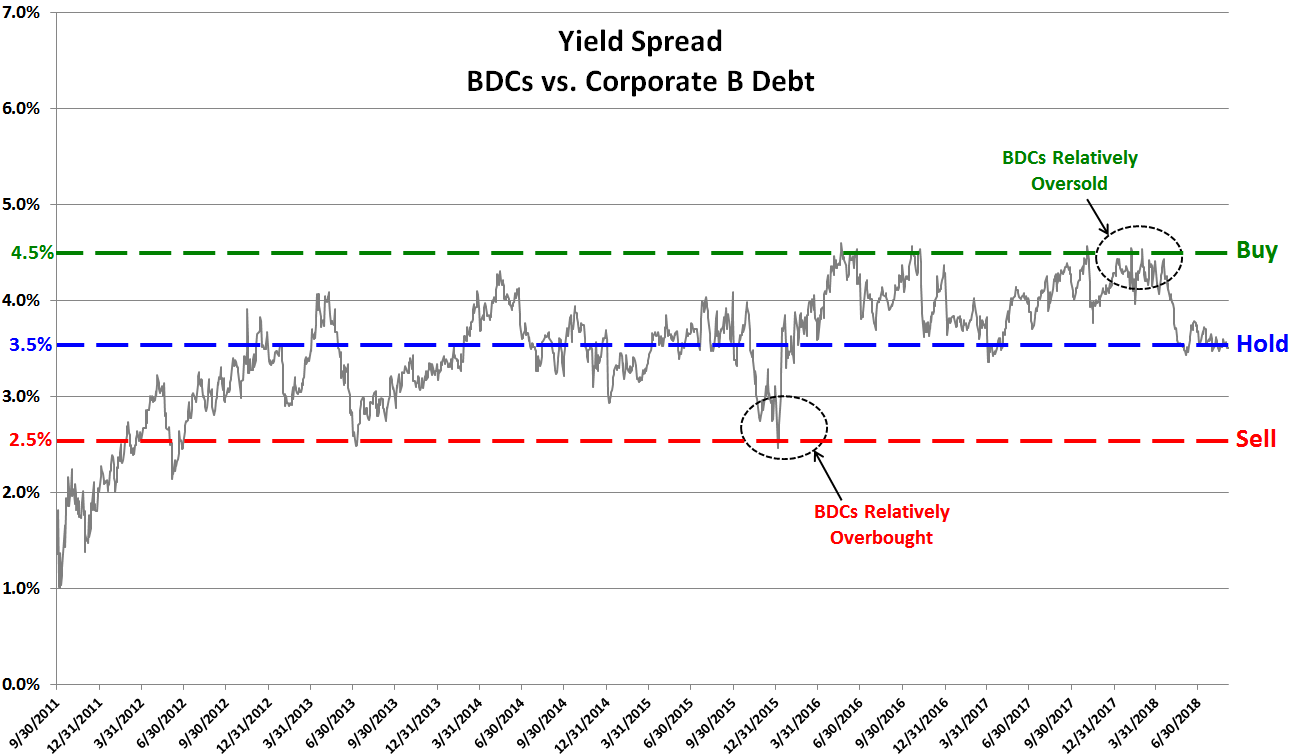

Source:

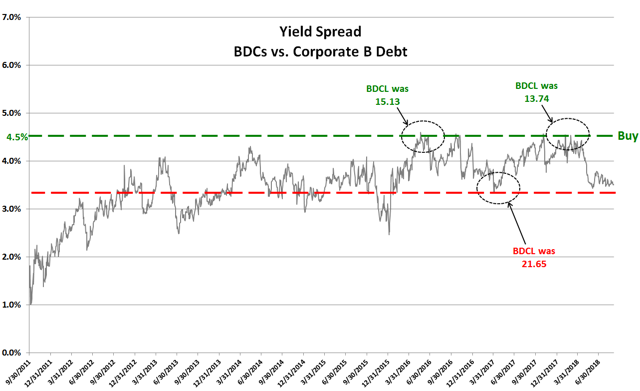

Source: