The following is a quick GSBD Update that was previously provided to subscribers of Premium Reports along with revised target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all business development companies (“BDCs”) please see Deep Dive Reports

Summary

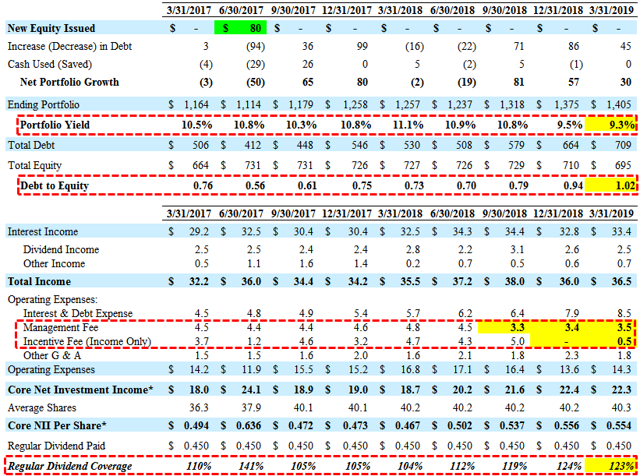

- GSBD beat best-case projections (again) mostly due to lower incentive fees paid during the quarter covering its dividend by 123% (average coverage of 117% over the last 8 quarters).

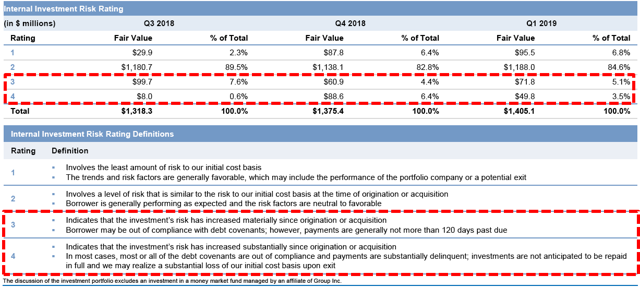

- NAV/share declined by 2.3% due to the restructuring of ASC Acquisition Holdings, discussed in the previous report and Country Fresh Holdings which was placed on non-accrual status.

- Country Fresh is also an investment held by PFLT that contributed to its recent NAV decline.

- Effective May 8, 2019, GSBD commenced the dissolution of its SCF and will receive around $216 million of assets financed directly on its balance sheet. This will instantly increase leverage and returns to shareholders as well as increase the amount of first-lien and overall diversification of the portfolio.

- NTS Communications remains on non-accrual representing 3.5% of the total investments and is expected to be repaid in Q2 2019. Excluding NTS, non-accruals represented less than 0.1% of the portfolio.

Goldman Sachs BDC (GSBD) beat best-case projections (again) covering its dividend by 123% mostly due to lower incentive fees paid during the quarter. The company has covered its dividend by an average of 117% over the last 8 quarters. The company is in the process of dissolving its Senior Credit Fund(“SCF”) and will receive around half of the assets financed directly on its balance sheet. Effective May 8, 2019, GSBD commenced the dissolution of the joint venture partnership and GSBD received its pro rata portion of the SCF investments on balance sheet. This will instantly increase leverage and returns to shareholders as well as increase the amount of first-lien and overall diversification of the portfolio.

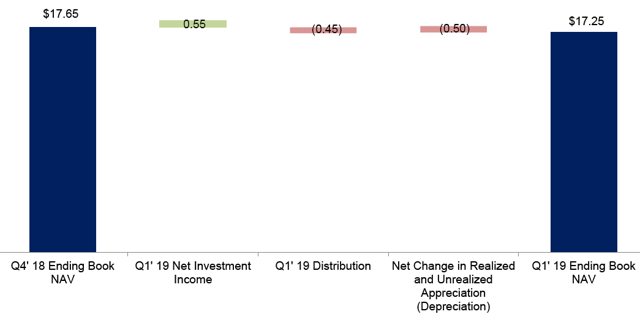

Net asset value (“NAV”) per share declined by $0.40 per share or 2.3% (from $17.65 to $17.25) due to the restructuring of ASC Acquisition Holdings, LLC(“ASC”) discussed in the previous report and Country Fresh Holdings which was placed on non-accrual status due to financial underperformance. Country Fresh is also an investment held by PennantPark Floating Rate Capital (PFLT) that contributed to its recent NAV decline.

In June 2018, shareholders approved the reduced asset coverage ratio of at least 150% (potentially allowing a debt-to-equity of 2.00) and management reduced the base management fee from 1.50% to 1.00%, lowering expenses and improving dividend coverage as shown below. GSBD is now well above its previous targeted leverage of 0.75 and has obtained all of the necessary approvals and is positioned to benefit from the reduced asset coverage requirement.

ASC Acquisition Holdings, LLC (“ASC”) was discussed on the previous call with management:

“Animal Supply is a more fluid situation but there are recent developments that we would like to share. Animal Supply is a nationwide distributor of pet food and supplies. Our investment thesis centered on the Company’s leading industry position and positive industry tailwinds driven by long-term trends driving demand for pet food supplies. During 2018 the Company’s performance and profitability declined. We determined that the best course of action was to deleverage the capital structure to better position the company to perform. As of last Friday, we successfully closed restructuring by swapping our debt for equity and providing additional working capital to enable the company to increase fill rates, revenue and EBITDA. We believe that with a clean balance sheet and a more focused management the Company is well positioned to benefit from stable industry trends and consolidation opportunities.”

During the previous quarter, Its first lien, last-out unitranche debt investment in NTS Communications, Inc. (“NTS”) was added to non-accrual status and represents 3.5% and 3.8% of the total investment portfolio at fair value and amortized cost, respectively. This investment is expected to be repaid in Q2 2019 in connection with the sale of NTS.

“However, the exact timing is dependent on the satisfaction of certain closing conditions to the sale transaction, including receipt of Federal Communications Commission approval.”

Excluding its investment in NTS, non-accruals represented less than 0.1% and 0.7% of the total investment portfolio at fair value and amortized cost, respectively.

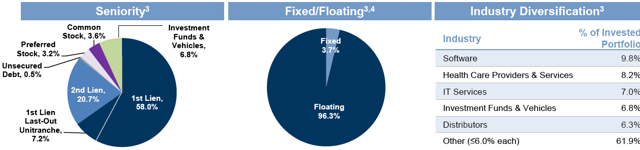

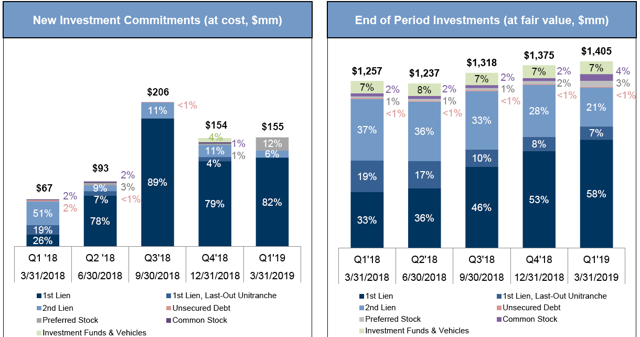

New investments during Q1 2019 were mostly first-lien and the portfolio remains heavily invested in first-lien debt including its SCF as shown below. Over the past four quarters, GSBD’s proportion of its first lien debt investments within its investment portfolio increased by 74% and second lien debt investments decreased by 44%.

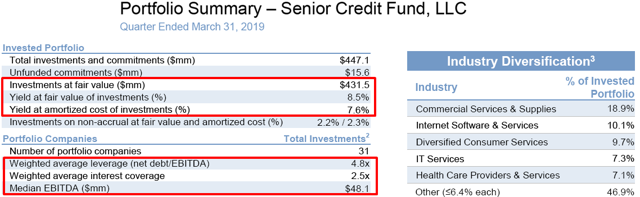

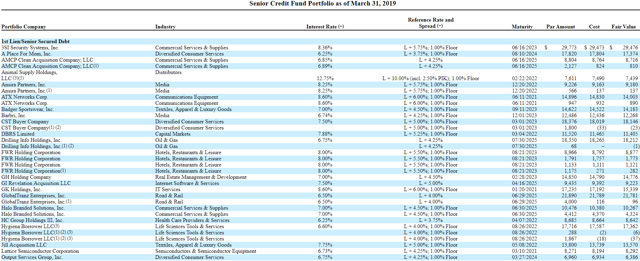

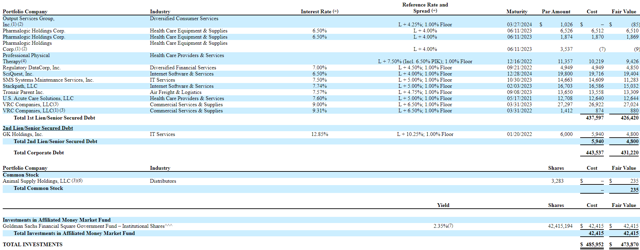

Senior Credit Fund (“SCF”) Portfolio

The SCF was GSBD’s largest investment and is a joint venture with the Regents of the University of California (“Cal Regents”) that invests primarily in senior secured loans to middle-market companies. GSBD and Cal Regents have both subscribed/invested $100 million and using off-balance sheet leverage have invested in 32 companies with a total fair value of almost $452 million. GSBD will directly invest in around 50% of the portfolio using its own leverage and likely selected the higher-yielding assets. The SCF portfolio is 95% first lien and 100% floating rate diversified by sector:

“On May 8, 2019, the Company and Cal Regents each contributed $125,555 to the Senior Credit Fund, which was used by the Senior Credit Fund to repay in full all outstanding indebtedness, including all accrued and unpaid interest and fees, under the Asset Based Facility and to fund certain other related expenses that the Senior Credit Fund expects to incur in connection with its dissolution. The Asset Based Facility was then terminated and all liens securing the collateral under the Asset Based Facility were released. The Company funded its portion of the contributed amount through additional borrowings under its Revolving Credit Facility.”

“Following the repayment and termination, the Senior Credit Fund distributed each member’s pro rata share of all of its assets (other than cash and cash equivalents), primarily consisting of senior secured loans, to the members. The Company also assumed the obligation to fund outstanding unfunded commitments of the Senior Credit Fund that totaled $7,795 as of March 31, 2019, representing 50% of the Senior Credit Fund’s aggregate unfunded commitments. The pro rata portion of the assets received by the Company will become the Company’s assets and will be directly included in the Company’s consolidated financial statements and notes thereto, and will also be included for purposes of determining the Company’s asset coverage ratio. Based on March 31, 2019 balances, the assets to be received by the Company are approximately $221,769 and $215,728 at amortized cost and at fair value, respectively. In connection with the repayment of the Asset Based Facility and the distribution of all of its loan assets, the Senior Credit Fund declared a $2,000 cash distribution to its members, representing estimated quarter-to-date net investment income, 50% of which will be paid to the Company.”

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.

For updated GSBD target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs please see Premium Reports.