The following is a quick FSK Update that was previously provided to subscribers of Premium Reports along with revised target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all business development companies (“BDCs”) please see Deep Dive Reports

Summary

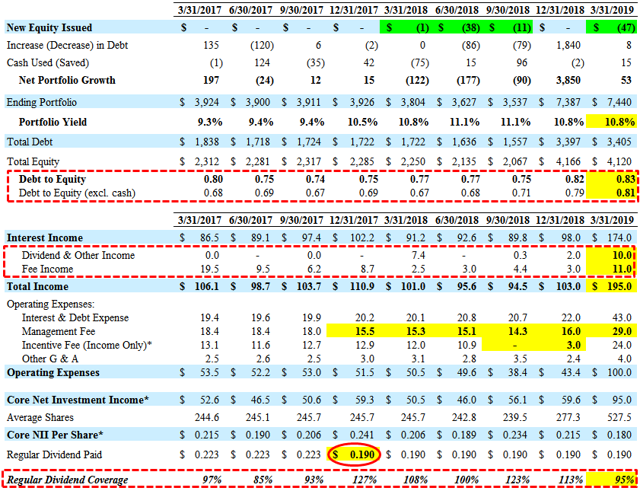

- This is the first full quarter of reported results after combining the CCT portfolio. FSK reported just below its base case projections covering 95% of its dividend.

- As mentioned in the previous report, Sungard Availability is filing for Chapter 11 and was marked down by around $2.7 million and added to non-accrual status in Q1 2019.

- Z Gallerie filed for Chapter 11 bankruptcy in March 2019 and marked down an additional $6.5 million during Q1 2019.

- Its non-accrual investment Charlotte Russe Inc. recently announced that it had sold the Charlotte Russe brand and related IP that will drive realized losses of around $20 million.

- The company is repurchasing shares. Non-accruals decreased from 1.0% to 0.4% of the portfolio and include many of the energy and retail-related investments discussed in the previous report.

FS KKR Capital Corp. (FSK) reported just below its base case projections covering 95% of its dividend. This was the first full quarter of reported results after combining the CCT portfolio and management is working to reduce the amount of non-income producing equity investments. FSK remains above its target debt-to-equity ratio of 0.75 due to the previous NAV declines. During Q1 2019, the company repurchased 7.4 million shares (~1.4% of available shares) at an average price of $6.33 (19% discount to NAV).

Michael Forman, Chairman and CEO. “During the first quarter, we made further progress on our long-term strategic initiatives, and continued improving upon our portfolio. We feel well positioned with our significant scale and quality deal flow, and believe our continued execution of our share repurchase program demonstrates our confidence and our commitment to aligning ourselves with our shareholders.”

Previously, I downgraded FSK due to continued credit issues as discussed in the previously linked Deep Dive report. FSK’s Board has declared a regular cash distribution for Q2 2019 of $0.19 per share, paid on or about July 2, 2019 to stockholders of record as of the close of business on June 19, 2019.

Total non-accruals decreased from 1.0% to 0.4% of the portfolio based on fair value partially due to ThermaSys Corp, MB Precision Holdings, and Aspect Software Inc. added back to accrual status. As mentioned in the previous report, Sungard Availability Services Capital (cost and fair value of $14.7 million and $4.8 million, respectively) is filing for Chapter 11 and was marked down by around $2.7 million and added to non-accrual status in Q1 2019. The other non-accruals include many of the energy and retail-related investments discussed in the previous report including AltEn, LLC, Hilding Anders, Rockport (Relay), Advanced Lighting Technologies Inc., Charlotte Russe Inc., CTI Foods Holding Co., Z Gallerie, Petroplex Acidizing Inc., and HM Dunn Co.

Z Gallerie filed for Chapter 11 bankruptcy in March 2019 and marked down an additional $6.5 million during Q1 2019. The company blames the filing on self-imposed problems namely a failure to invest enough in e-commerce, the addition of a costly distribution center and an expansion that didn’t meet performance targets. On March 20, 2019 Nine West Holdings announced its exit from Chapter 11 that will not impact upcoming NAV but will likely result in realized losses of around $6.5 million in Q2 2019. Its non-accrual investment Charlotte Russe Inc. recently announced that it had sold the Charlotte Russe brand and related intellectual property to YM Inc. that will drive additional realized losses of around $20 million.

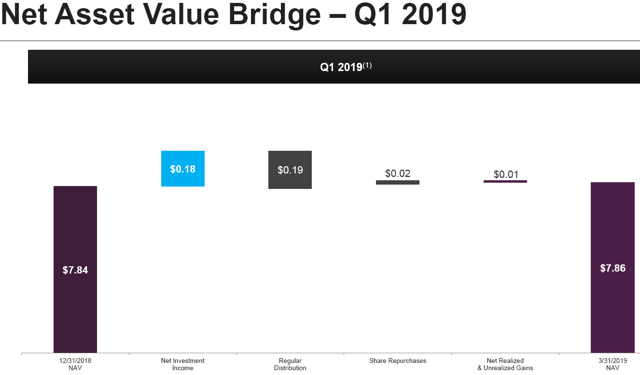

During Q1 2019, net asset value (“NAV”) per share increased by $0.02 or 0.3% (from $7.84 to $7.86) due to share repurchases as the net unrealized gains were offset by under-earning the dividend.

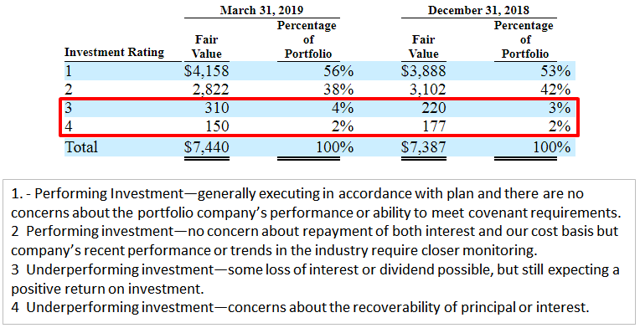

There was a $90 million increase in the amount of investments in ‘Investment Rating 3’ implying “Underperforming investment some loss of interest or dividend possible, but still expecting a positive return on investment” and needs to be watched.

In December 2018, FSK’s board of directors authorized a $200 million stock repurchase program. During the three months ended March 31, 2019, the Company repurchased 7,396,048 shares of common stock pursuant to the share repurchase program at an average price per share (inclusive of commissions paid) of $6.33 (totaling $47 million). During the period from April 1, 2019 to May 7, 2019, the Company repurchased 1,429,956 shares of common stock pursuant to the share repurchase program at an average price per share (inclusive of commissions paid) of $6.27 (totaling $9 million). Additional repurchases could be limited due to being above target leverage but funded through rotating out of portfolio assets.

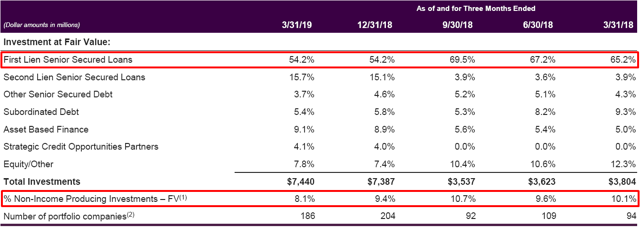

As mentioned earlier, management has been working to reduce the amount of non-income producing equity investments that is now 8.1% of the portfolio (partially due to markdowns in equity investments). However, the amount of first-lien declined from 70% to 54% due to combining the portfolios of FSIC and CCT:

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.

For updated FSK target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs please see Premium Reports.