The following is a quick TSLX Update that was previously provided to subscribers of Premium Reports along with revised target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all business development companies (“BDCs”) please see Deep Dive Reports

Summary

- On February 18, 2019, PayLess Inc. filed for Chapter 11 and during Q2 2019, its $14 million ABL term loan was repaid in full resulting in 18% IRR and taken into account with the updated projections.

- As predicted, its $25 million ABL-DIP loan to Sears was fully repaid in connections with the bankruptcy court approving the sale of its assets to ESL Investments for $5.2 billion. However, TSLX invested an additional $75 million in Q1 2019.

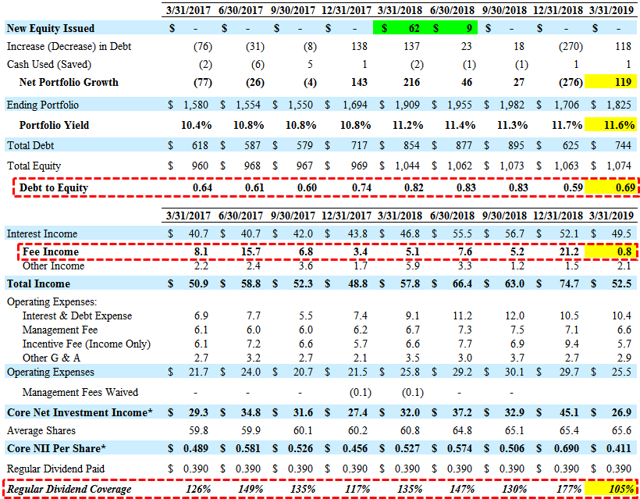

- For Q1 2019, TSLX reported just below base case due to continued lower leverage and much lower-than-expected “other fees” income which includes prepayment fees and accelerated amortization of upfront fees.

- Credit quality remains solid with 100% performing portfolio of 97% true first-lien. NAV per share increased by 0.6% partially due to unrealized appreciation “primarily due to a tightening spread environment and positive credit-related adjustments.”

- The Board adjusted the 10b5-1 Repurchase Plan to allow for repurchases “just below 1.05x the most recently reported net asset value per share, less the amount of any supplemental dividend declared for that quarter” which is around $17.15.

- Previously, TSLX increased its target debt to equity target range from 0.75x-0.85x to 0.90x-1.25x potentially driving a quarterly dividend increase from the current $0.39 to between $0.45 and $0.55 depending on leverage and new asset yields.

TSLX Dividend Coverage Update:

TSLX has covered its regular dividend by an average of 140% over the last four quarters, growing undistributed taxable income and capital gains to $1.19 per share.

“As we said before, if we believe there is a sustainable increase in the earnings power of the business by operating in our target leverage range for an extended period of time, then we would look to resize our base dividend in context of the underlying earnings power of the business to ensure we’re optimizing cash distribution and satisfying risk related distribution requirements. We will continue to monitor undistributed taxable income and gains closely as part of our ongoing review of our distribution strategy.”

The company only experienced $33 million of repayments and exits during Q1 2019 resulting in lower “other fees” income which includes prepayment fees and accelerated amortization of upfront fees. This along with lower leverage were the primary drivers for lower dividend coverage in Q1 2019 and special/supplemental dividend of $0.01 per share payable in June which was below the base case projected.

“Total investment income was $52.5 million, down from $74.7 million in the prior quarter, primarily due to elevated level of activity-related fees earned during Q4. Interest and dividend income was $49.5 million, down $2.5 million from the previous quarter given a slight decrease in the average size of our investment portfolio. Other fees, which consist of prepayment fees and accelerated amortization of upfront fees from unscheduled paydowns were $0.8 million compared to $21.2 million in the prior quarter, which experienced record high repayment levels.”

For Q1 2019, TSLX reported just below base case projections due to continued lower leverage and much lower-than-expected fee income during the quarter but covering its dividend by 105%. Previous quarters typical have higher “other fees” income which includes prepayment fees and accelerated amortization of upfront fees. Annualized ROE for the first quarter 2019 was 10.0% and 14.5% on a net investment income and a net income basis, respectively.

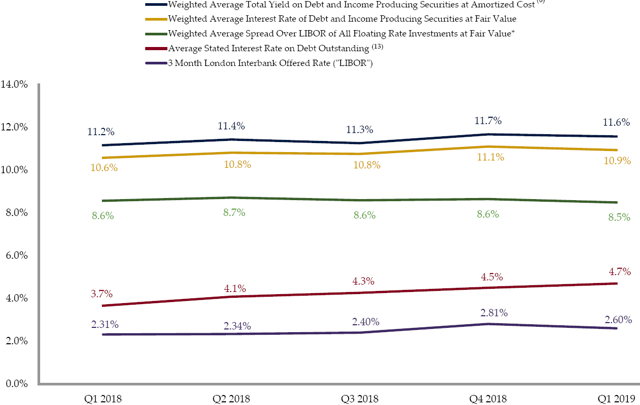

During Q1 2019, there was a slight decline in its portfolio yield (from 11.7% to 11.6%) due to new investments at lower yields.

TSLX management continues to produce higher returns by investing in distressed companies through excellent underwriting standards that protect shareholders during worst-case scenarios including call protection, prepayment fees and amendment fees backed by first-lien collateral of the assets. Historically, higher returns have been partially driven by these strong financial covenants and call protections during periods of higher amounts of prepayments (discussed below) and worst case scenarios. However, similar to previous reports, the base case projections do not include large amounts of fee and other income related to early repayments.

“At quarter end, nearly a 100% of our portfolio by fair value was sourced through non- intermediary channels. This allows us to structure meaningful downside protection on our debt investments. To provide some numbers around this, at quarter end we maintained effective loading control on 81% of our debt investments average 2.1 financial covenants per debt investment and had meaningful call protection on their debt portfolio of 103.4 as a percentage of fair value as a way to generate additional economics as our portfolio get repaid in the near term.”

TSLX Risk Profile Update:

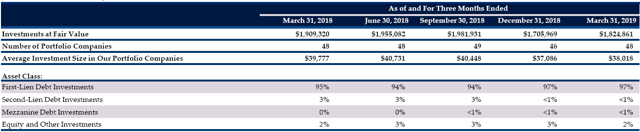

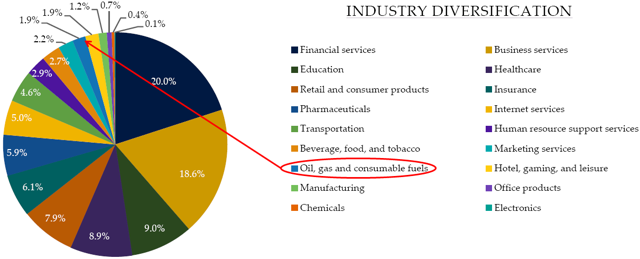

As of March 31, 2019, 100% of the portfolio was meeting all payment and covenant requirements. First-lien debt remains around 97% of the portfolio and management has previously given guidance that the portfolio mix will change over the coming quarters with “junior capital” exposure growing to 5% to 7%.

“As of March 31, 2019, the portfolio based on fair value consisted of 97.4% first-lien debt investments, 0.2% second-lien debt investments, 0.1% mezzanine debt investments, and 2.3% equity and other investments.”

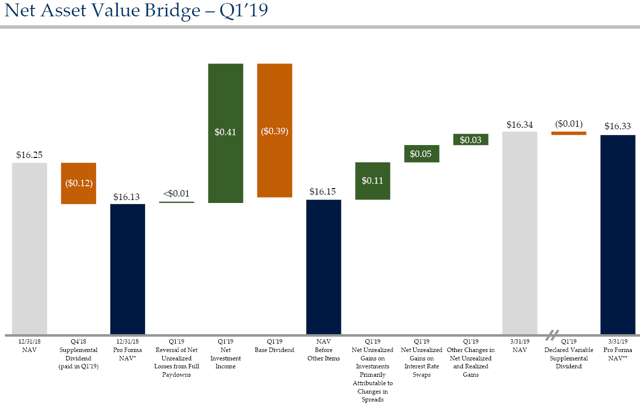

As predicted, net asset value (“NAV”) per share increased by $0.09 or 0.6% (from $16.25 to $16.34) partially due to unrealized appreciation that “resulted from an increase in fair value, primarily due to a tightening spread environment and positive credit-related adjustments.”

“The difference between this quarter’s net investment income and net income was primarily driven by unrealized gains of $0.11 per share from the impact of tightening credit spreads and the valuation of our portfolio and mark-to-market gains of $0.05 per share related to our interest rate swaps from the flattening of the forward LIBOR curve. Reported net asset value per share at quarter end was $16.34, an increase of $0.21 compared to the prior quarter after giving effects of the impact of the Q4 supplemental dividend which was paid during Q1. Net asset value movement this quarter was primarily driven by unrealized gains related to a partial recovery of credit spreads following year-end volatility and the flattening of the forward curve as discussed.”

On February 18, 2019, PayLess Inc. filed for Chapter 11 and during Q2 2019, its $14 million ABL term loan was repaid in full resulting in 18% IRR and taken into account with the updated projections:

“On February 18, 2019, Payless filed voluntary petition for relief under Chapter 11 of the bankruptcy code given the continuing challenges facing brick and mortar retailers. Post quarter end, we were fully repaid on our loan which resulted in an unlevered – gross unlevered IRR of 18% on our investment.”

It is important for investors to understand that one of TSLX’s strategies for higher IRRs is investing in distressed retail asset-based lending (“ABL”) as “traditional brick and mortar retail gives way to the rise of e-commerce”. Historically, borrowers have paid amendment fees to avoid even higher prepayment fees if they decided to refinance. Also, the amendments included additional “borrowing base” providing increased downside protection on the investment. This strategy continues to drive higher fee income including prepayment and amendments fees. See the end of this report for previous examples.

“Retail ABL continues to be one of our various themes given the ongoing secular trends in our platform’s differentiated capabilities and relationships in this area. As the direct lending asset classes become increasingly competitive, we have continually developed and evolved our investment themes in order to generate a robust pipeline of strong risk-adjusted return opportunities.”

“What really matters is, how we think the inventory will liquidate as it compares to what – where we are lending against it. Retail goes as well as the consumer. That is not the – that’s not what’s happening here, right. Consumer is in good health. There is a business model issue and a structural issue with retail, but more so given the fixed cost base and given the discerning mediation of both kind of fast brands and plus Amazon and omni-channel business models. And so, it’s really the liquidation value of inventory and the liquidation value of the inventory has held up great. So, we continue to hope for a decent amount of structural change. So we can provide capital and provide – be a solution provider into that space. And quite frankly, the liquidation values continue to hold up very, very, very well.”

From previous call: “35% of our 2018 originations were what we call opportunistic capital deployment in areas where our platform’s ability to underwrite and navigate complexity and process risk, allow us to create excess returns across our portfolio. Examples since inception include our investments in upstream E&P, retail ABL and secondary market purchases during periods of market volatility. These also include opportunities arising from the challenging regulatory environments for banks such as our larger financings iHeart and Ferrellgas. Since inception through year-end 2018, the gross unlevered IRR in our fully realized investments that we designate as opportunistic in nature was 28%, which compares to a gross unlevered IRR of 14% across the remainder of our fully realized investments over this period of time.”

As predicted, its $25 million ABL-DIP loan to Sears was fully repaid in connections with the bankruptcy court approving the sale of its assets to ESL Investments for $5.2 billion. However, TSLX invested an additional $75 million in Q1 2019 for “a strong risk-adjusted return opportunity for our shareholders”:

“During the quarter, we also received full repayment of our Sears DIP loan in connection with the company’s exit from chapter 11. Subsequently, we participated in a $250 million asset-based loan to support Sears’ go-forward operations. We’ve been a lender to the company since late 2015. Given our relationship and familiarity with the company’s capital structure and its collateral, we believe we created a strong risk-adjusted return opportunity for our shareholders.”

“Specifically with Sears and generally with all of our asset-based loans which is quite frankly this hasn’t to anything about the prospects of any of our retail asset-based loans, but we underwrite them to liquidation value. I think our last dollar is 80% of NRLV, liquidation value of the inventory, which hold up very, very well and when most of the stores were liquidated, in the all series format. So, again, this is not commenting on Sears specific prospects. We continue to believe that all brick and mortar retail is extremely challenged. But you would expect, we underwrite these transactions to a liquidation given the secular challenges and the volatility of earnings and the fixed cost structure that exists in all brick and mortar retail. So that is actually very similar on a structure basis with the same protections and borrowing-based mechanism that you had and advance rate that you had in the last years.”

“On February 18, Payless filed voluntary petition for relief under Chapter 11 of the bankruptcy code given the continuing challenges facing brick and mortar retailers. Post quarter end, we were fully repaid on our loan which resulted in an unlevered – gross unlevered IRR of 80% on our investment.”

Similar to investing in distressed retail assets, the company is focused on increasing returns through investing opportunistically in oil/energy but only first-lien “with attractive downside protective features in the form of significant hedged collateral value at current price levels”. Management has mentioned that energy exposure would not exceed 10% of the portfolio and only first-lien using appropriate hedges. As discussed in previous reports, TSLX made “opportunistic” investments in MD America Energy during Q4 2018, Ferrellgas Partners during Q2 2018 and Northern Oil & Gas in Q4 2017 that was previously repaid.

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.

For updated TSLX target prices, dividend coverage and risk profile rankings, credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions on all BDCs please see Premium Reports.

I was a client of yours for years but somehow we became disconnected. Perhaps the credit card being used expired, I don’t really know. How do we reconnect.

Charles Torrey

Charles – I sent you an email about your subscription.