The following is a quick MRCC Update that was previously provided to subscribers of Premium Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

MRCC Risk Profile Update:

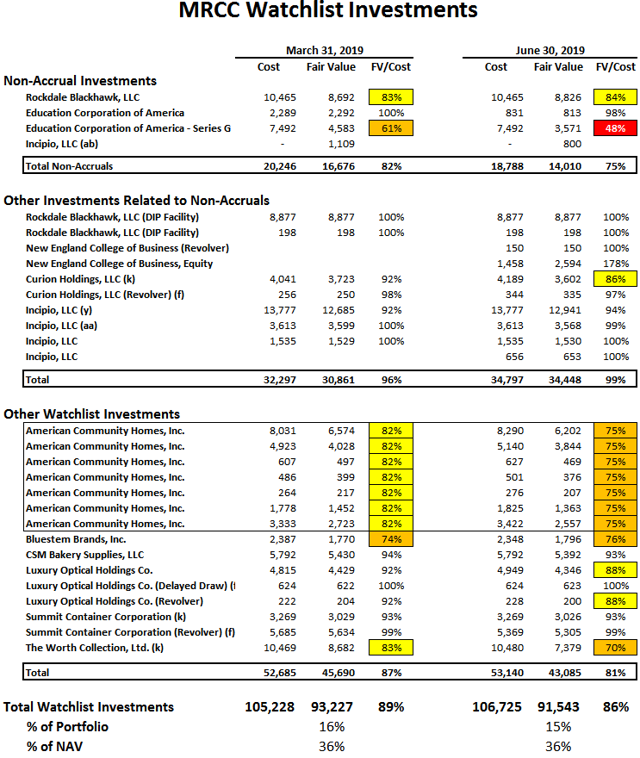

As mentioned in the BDC Risk Profiles report, MRCC was downgraded last year due to potential/continued credit issues including adding Education Corporation of America (“ECA”) to non-accrual status, previous markdowns of Rockdale Blackhawk and realized losses from TPP Operating, Inc. During Q2 2019, its net asset value (“NAV”) decreased by $0.15 or 1.2% (from $12.67 to $12.52) mostly due to additional markdowns in previously discussed investments including American Community Homes, Inc. (“ACH”) as well as its retail-related investment in The Worth Collection, Ltd.

My primary concern is the potential for additional non-accruals and markdowns of the investments listed in the previous table that currently account for around 15% of the portfolio and 36% of NAV per share. The worst-case projections take into account additional credit issues that could result in a dividend reduction of around 25% as discussed later.

“We’re in an uncertain market and things are happening very often beyond our control as investors. And some of the things that happen from time to time that are beyond our control very really affect industries, in particular, companies in those industries, and it’s very hard to predict. So, we’re going to continue to do that, and we’ll be back to you next quarter with a report. Hopefully, we’ll see more stability in world affairs and other things that are happening that are the more uncontrollable factors.”

The total fair value of investments on non-accrual declined to $14.0 million (previously $16.7 million) and account for around 2.2% of the portfolio fair value and $0.69 per share or around 5.5% of NAV. ECA was added to non-accrual status during Q4 2018 and are ‘junior secured loans’ and preferred stock as compared to first-lien positions. Other non-accruals include its Curion Holdings promissory notes, Incipio, LLC third lien tranches, Millennial Brands LLC (previously Rocket Dog Brands LLC), and Rockdale. The Curion promissory notes and the Incipio third lien tranches were obtained in restructurings during 2018 for no cost.

“The other non-accruals just as a reminder, because this is a constant source of confusion. We have a couple of names where a portion of the holding is on non-accrual because there are situations in which we took over a piece of debt or a piece of paper that we didn’t pay for as part of a restructuring. That includes the promissory note at Curion and a third lien piece at Incipio, and those are the only parts of those that are on non-accrual. There was really no cost associated with those two. And so I don’t know. The only time those would ever really go in accrual would be, if there was a massive recovery in the business. But because those are no cost, I mean, it doesn’t make any sense to put them on accrual status. And then there’s a small piece of preferred Millennial Brands that we don’t really expect to ever see value from. Those are all the non-accruals.”

During Q2 2019, MRCC participated in a credit bid to acquire the assets of New England College of Business (“NECB”), which was a subsidiary of ECA resulting in a 20.8% equity stake in NECB in exchange for a $1.5 reduction of secured loan position in ECA. Management mentioned “the ECA situation is going to be ongoing for an [extended] period of time”:

Q. “A quick on Education Corporation of America, can you give like just some color on what drove the write-down there this quarter and then the outlook for just the rest of your non-accruals in general and the timing of the resolution?”

A. “So, yeah, I think what you have to look at there is ECA has basically been split into two investments now. So that’s the confusion here. ECA had an asset that’s called NECB, New England College of Business, which is a performing school that’s was – that’s doing okay and was a good ongoing asset. And so basically, through the receivership situation there, we’ve credited a bit some of the debt and taken over NECB. So when you look at the marks, you sort of have to look at it by combining ECA and NECB. And more or less, when you look at it that way, the valuation hasn’t really changed quarter-to-quarter. The ECA situation is going to be ongoing for a period of time, that’s going to be extended”

As discussed in previous reports, American Community Homes, Inc. (“ACH”) is still on accrual status (discussed later) and needs to be watched as it still accounts for around $0.73 per share or 5.9% of NAV. In October 2014, MRCC funded a senior credit facility to support the recapitalization of Towne Mortgage Corporation by ACH. Based in Troy, Michigan, Towne originates and services mortgage loans on residential properties located primarily in Michigan, Minnesota and Wisconsin. ACH has been marked down in previous quarters and during Q1 2019, MRCC invested another $3.3 million. Also mentioned in the previous report, MRCC has put in place new management and was discussed on a previous call:

“American Community Homes just to be more clear is that was a compliance in the mortgage servicing business and general the mortgage servicing rights on a fair value from dollar in the industry and so what we did and our third-party valuation firm did more importantly is they looked at industry norms for valuation of mortgage servicing rights there. You know I don’t believe that there is any deterioration in the overall enterprise value or the value of the Company, but when you value particular companies based on underlying rights or commodity items its right to do what they did. So we took the adjustment on that, but at the end of day as you mentioned, we have no additional non-accrual and I believe our portfolio is stable. There has been a change in management, we have put a new management, there is some things that could be done on the operating basis to make a company more profitable and better, we feel we have done all that and from here it looks really good in terms of the company’s valuation. We feel solid in the future should be very strong, because we have done a lot to change the management team there and how they approach the business and it looks good in the future even if we have a protracted slowdown in mortgage originations, which appears to be the case right now. We still think there is value being created in the business.”

Previously, management discussed its investment in ACH including having “significant downside protection” and “our expectation is that the company can be improved and that we will enjoy a full recovery”:

From previous call: “Our expectation is that we have significant downside protection through this fairly large portfolio of mortgage servicing rights, the only trouble of the business is because the mortgage origination business is slow and liquidity became a little tight it’s harder for the company to retain as many new mortgage servicing rights as they would have liked, which would have created a more value for us. But long-term, we expect the recovery here, sponsor here has made significant changes to management and as advisors in who have made fairly large cost cuts to the business, which we don’t think will impact the business profitability going forward negatively, but only positively. And our expectation is that the company can be improved and that we will enjoy a full recovery. And we also have some equity in this business as well, which has some potential upside in the future as well, but for now this is the fair market value on the loans. There were some additional funding I mentioned on the term loan during the period, which is what you are seeing with regards to the increase in funding.”

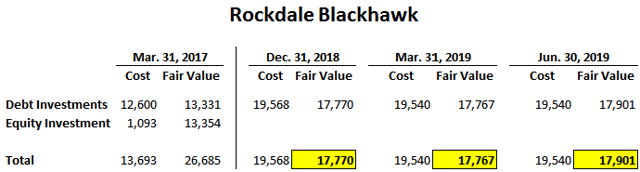

The fair value of its investment in Rockdale Blackhawk, LLC (“Rockdale”) remained stable but previously filed for bankruptcy as part of a restructuring process. MRCC’s total investment in Rockdale accounts for almost $18 million (around 2.8% of the portfolio) and $0.88 (or 7.0%) of NAV per share. Management

Q. “The fair value in Rockdale went up a little quarter-over-quarter, was that simply change in the discount rate?”

A. “It’s really in the margin, I think. It’s not a particularly material change. So, I wouldn’t read much into it. It’s just as you go through sort of a waterfall analysis and look at how things sort of play out on the valuation side, they have small shifts up and down. So there was some, I think, in the estate some realization of certain assets in the estate, so that has something to do with it as well. The Rockdale situation ought to have some resolution in the next quarter or two. It’s – the arbitration there is happening as we speak, and we’ll see – it’ll take some time for that case to get through all the arguments, and then the arbitrator has some time to make a decision on what he wants to do. So I would expect to see that resolve itself, if not in the third quarter, maybe into the early part of the fourth quarter.”

Previously, management mentioned that its Rockdale investment was valued appropriately but that “there is a range of outcome some of which are considerably higher and some of which are lower”:

From previous call: “We are required to mark every assets to what we believe is a fair market value in every quarter, based on the available information. And we use independent third-parties to assist us in that and we have done nothing different this period than any other period and nothing different with this investment than other investments. We have given all the information we have to an independent third-party evaluation firm who has done What Ted has described, which is try to put reasonable probability of outcomes on the assets and the liquidation of assets and the recovery of assets and sales of business units and things of that nature. And I will just say probably there is a range of outcome some of which are considerably higher and some of which are lower. So, this is the best expectation of what we think the fair value of the loan is today based on the view of the independent third-party and all the contingencies.”

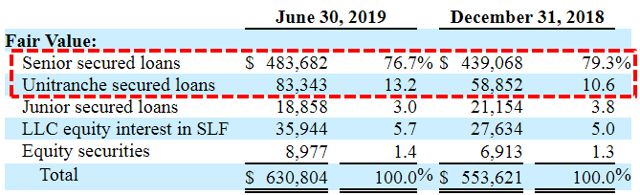

MRCC’s portfolio remains primarily of first lien loans, representing around 90% of the portfolio and its investment in the SLF (discussed next) remains around 6% of the portfolio:

“Our portfolio is heavily concentrated in senior secured loans, and specifically first lien secured loans. 92.9% of our portfolio consists of secured loans, and approximately 90% is first lien secured. We are pleased with the construction, diversity and the senior secured nature of our investment portfolio at this point in the credit cycle.”

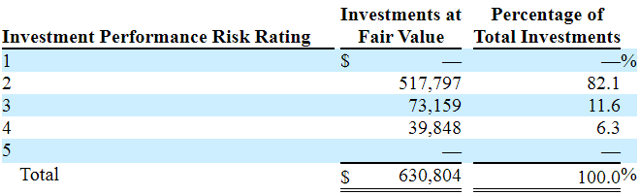

Grade 4: Includes an issuer performing materially below expectations and indicates that the issuer’s risk has increased materially since origination. In addition to the issuer being generally out of compliance with debt covenants, scheduled loan payments may be past due (but generally not more than six months past due). For grade 4 investments, we intend to increase monitoring of the issuer.

Grade 5: Indicates that the issuer is performing substantially below expectations and the investment risk has substantially increased since origination. Most or all of the debt covenants are out of compliance or payments are substantially delinquent. Investments graded 5 are not anticipated to be repaid in full and we will reduce the fair market value of the loan to the amount we expect to recover.

MRCC Dividend Coverage Update:

MRCC was previously downgraded in the Dividend Coverage Levels report due to continued credit issues driving increased reliance on fee waivers to cover its dividend. Over the last three quarters, the company has covered its dividend only due to the ability to use higher leverage through its SBIC license and management willing to waive incentive fees to ensure dividend coverage. Previously, MRCC had higher dividend coverage only due to the ‘total return requirement’ driving no incentives fees paid. The following was from a previous earnings call:

“It has everything to do with where the NAV of the portfolio is in any given quarter and the performance on NII and dividends paid to shareholders. So it just depends on what happens each quarter going forward. And it’s a formulaic, as you said it’s formulaic. And so it’s difficult for me to predict today with any certainty where incentive fees would be on. And as you probably know it’s not a binary trigger either. They could be on it partially, or they could be on fully. It just depends on where we are with regards to NAV. It’s possible, there could be some incentive fee earned in the first quarter, if NAV was flat. I wouldn’t expect we’d be in a position to earn an entire incentive fee. And I would think that everything else was equal than probably in the second quarter is when you could start seeing an incentive fee payable.”

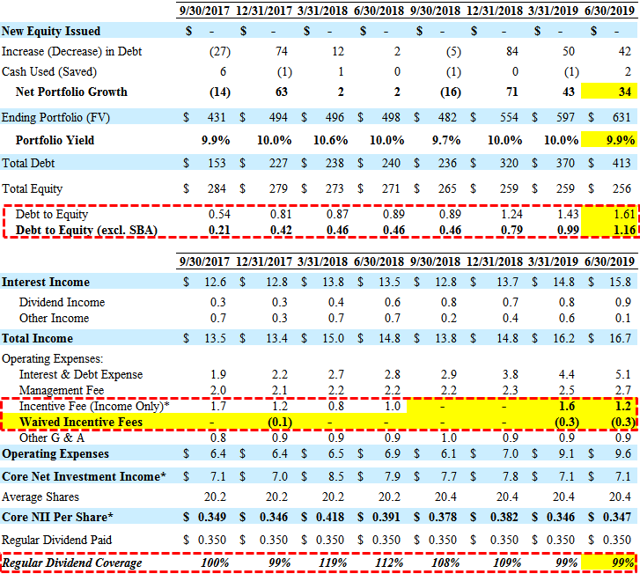

The last two quarters of higher-than-expected portfolio growth have driven its debt-to-equity ratio from 1.24 to 1.61 and its regulatory debt-to-equity ratio (excluding SBA debentures) has increased from 0.79 to 1.16. However, dividend coverage has not improved due to additional non-accruals and restricted cash which was discussed on the recent call:

“I think, if you look at where we are in NII coverage today and if all things being equal, if we could get the cash to work in the SBIC subsidiary, which we’re working hard to do, and if we could try to get some of the money that’s locked up in non-accruals out and reinvest it in accrual assets, our visibility for coverage looks really good.”

“What we’re trying to work on doing is getting some of the cash that’s sitting in the SBIC today to work over the next couple of three quarters. Obviously, it’s difficult to find deals in a competitive environment that are SBIC eligible. But we’re hopeful that we can find some good deals in the pipeline, and there are a couple now that look like they could qualify, and so getting that cash to work is really going to be a good help in driving NII performance, because right now, we’re just sitting on cash.”

Management also mentioned increasing its regulatory debt-to-equity ratio to 1.25 to 1.30:

“We’ve said for a while since the change in the rules that we intended to go above 1:1. So that shouldn’t be a big surprise. Maybe the velocity with which we were able to do it is surprising to you, but it’s not surprising to me because Monroe has always had a very, very active pipeline. We are, I believe, taking on deals that are maybe on the margin less risky than what we had done in the past. And we continue to expect to grow our regulatory leverage over the next couple of quarters, I’d say. I don’t know where we’ll wind up. It really depends on how the portfolio shakes out in the new origination shakeout, but I’d say think of it as maybe up to 1.25 to 1.3 times kind of regulatory leverage as a next target.”

As mentioned earlier, my primary concern is the potential for additional non-accruals and markdowns of certain investments that currently account for around 15% of the portfolio and 36% of NAV per share. The worst-case projections take into account additional credit issues and could result in a dividend reduction of around 25% as “the Board will revisit it in the future, and we’ll continue to think about it and look at it”:

From previous call: “We continue to believe that our adjusted NII can cover our dividend assuming no other material changes in our portfolio.”

“A lot of BDCs have cut dividends over the last several years. We never cut a dividend. We’ve only increased it once and have never cut. If we can cover the dividend and continue to cover it with room, over a long period of time, I feel like we’re doing a pretty good job for shareholders. But we’ll watch it, we’ll monitor it. And the Board will revisit it in the future, and we’ll continue to think about it and look at it. But to-date, we haven’t made a determination.”

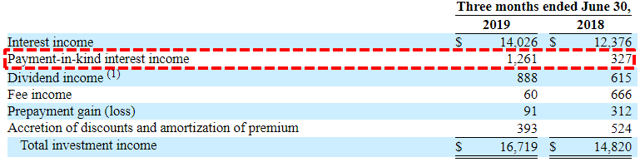

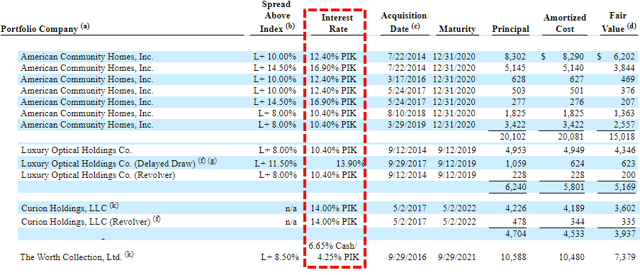

It should also be noted that there has been a meaningful increase in the amount of non-cash payment-in-kind (“PIK”) interest income from around 2.2% to 7.5% and included many of the “watchlist” investments discussed earlier including American Community Homes, The Worth Collection, Luxury Optical Holdings, and Curion Holdings:

Management was asked about potentially lowering the fees paid to management based on higher leverage and the response was mixed:

Q. “with the increased leverage, you’re talking 1.25 and maybe, obviously, you can go up to 2, but I know you wouldn’t take it there. But obviously, it drives more assets, and I know other BDCs have reduced some of their management fees for assets above the 1:1 ratio. I mean have you given that kind of any thought of reducing the base management fee on any level of assets?”

A. “Yes. So we’re really focused on delivering returns to shareholders in the form of NII-covering dividend. And so, what we have chosen to do to date is to look at waiving fees voluntarily to make sure we’re covering. And we’re going to continue to monitor, sort of, our performance level, and we’ll make decisions about that in the future if we think that it’s warranted based on our ability to cover. You got to remember that we have a business model, as Ted just went through, that includes a lot of people. We’ve really invested in infrastructure of people here to generate the unique deal flow. And I think if you look at a lot of other BDCs our size, you’ll find that their employee base is considerably smaller than ours.”

The company still has around $0.48 per share of undistributed net investment income for temporary dividend coverage shortfalls. For the quarter ended June 30, 2019, MRCC reported slightly below base-case projections with continued portfolio growth and expected slightly lower portfolio yield mostly covering its dividend for the 21st consecutive quarter.

Theodore L. Koenig, CEO: “We are pleased to report another quarter of consistent net investment income, with Adjusted Net Investment Income of $0.35 per share, representing the 21st straight quarter where per share Adjusted Net Investment Income met or exceeded our quarterly per share dividend. We have also made our 27th consecutive quarterly dividend payment to our shareholders. As of quarter end, our portfolio totaled $630.8 million in investments at fair value, which represented a $33.9 million increase in the portfolio during the second quarter, or about a 6% increase. Portfolio growth during the quarter was funded primarily utilizing the available capital under our revolving credit facility. We would expect to continue to selectively grow our portfolio, including utilizing additional leverage capacity available to us under our revolving credit facility. We would expect recent and continued portfolio growth to positively contribute to our earnings in future quarters.”

This information was previously made available to subscribers of Premium BDC Reports, along with:

- MRCC target prices and buying points

- MRCC risk profile, potential credit issues, and overall rankings

- MRCC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.