The following is from the AINV Quick Update that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

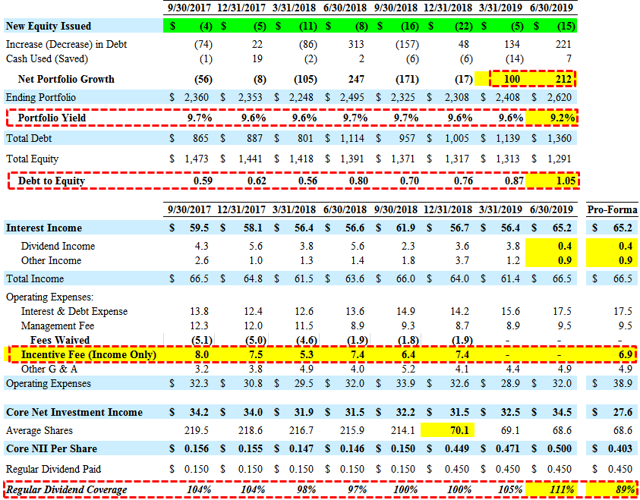

For calendar Q2 2019, Apollo Investment (AINV) reported between its base and best-case projections, covering its dividend but only due to no incentive fees paid during the quarter due to the ‘total return hurdle’. As shown in the following table, the company would have only covered 89% of its dividend if the incentive fees had been paid. This would imply that the company could have dividend coverage issues over the coming quarters depending on the progress of portfolio rotation out of non-income producing assets but also maintaining its portfolio yield and increased leverage to support portfolio growth. The Board maintained its distribution of $0.45 per share payable on October 5, 2019, to shareholders of record as of June 20, 2019.

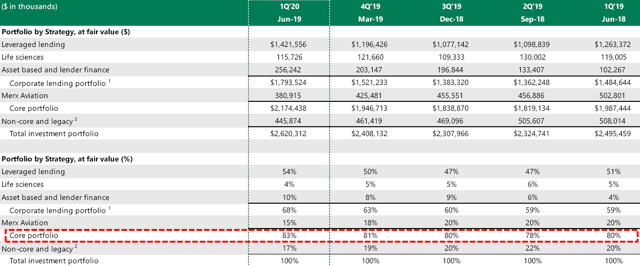

Mr. Howard Widra, AINV’s CEO commented, “During the quarter, we had substantial portfolio growth resulting from robust origination activity. This origination activity, in a competitive market, is another indication of the strength of our origination platform. Consistent with our plan, the growth was in lower risk corporate loans which further diversified the portfolio. Also, consistent with our plan, we reduced the size of our investment in Merx Aviation to less than 15% of the total portfolio and reduced non-core assets to 17% of the portfolio. Net investment income was strong for the quarter benefiting from the net growth in the portfolio, the impact from the total return provision in our fee structure, and the catch-up income from an investment being restored to accrual status.

I was expecting at least another $4.5 million credit to the incentive fees for calendar Q2 2019 as discussed on the previous call:

“So if you kind of take that versus a $55 million number that’s kind of carrying forward, we will kind of in our next quarter have some benefit from that carryover via the incentive fee credit. So, we have $55 million and 20% of that is $11 million, $6 million or $7 million of that was credited in the first quarter. So there’s still a performance – if nothing else changes this quarter there is another $4 million to $4.5 million of benefit in the second quarter.”

However, there were additional credit issues (Spotted Hawk and KLO Holdings as discussed later) resulting in no incentive fees paid during the quarter. As mentioned in the previous report, my primary concern is the ability of the company to cover the dividends during the last half of the year.

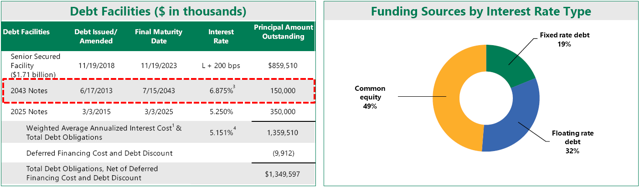

Portfolio growth was higher-than-expected and the company repurchased 0.9 million shares at a 16% discount to the previously reported net asset value (“NAV”) resulting in an increased debt-to-equity ratio of 1.05 as the company utilizes its access to higher leverage effective April 4, 2019. The company recently amended its Senior Secured Facility increasing commitments by $70 million which increased the size of the facility to $1.71 billion. In July 2019, the company announced the redemption of its 6.875% senior unsecured Baby Bond due July 2043 and is referenced in the BDC Google Sheets.

“We continue to manage our liabilities and optimize our capital structure. We increased the size of our revolving credit facility by $70 million during the quarter and subsequent to quarter end, we announced that we would be redeeming our 2043 unsecured notes.”

NAV per share declined by $0.06 or 0.3% (from $19.06 to $19.00) due to some markdowns mostly related to non-accruals including Spotted Hawk discussed in previous reports and KLO Holdings that was added to non-accrual status during the quarter. These unrealized losses were partially offset by accretive share repurchases (adding $0.04 per share) and overearning the dividend by $0.05 per share.

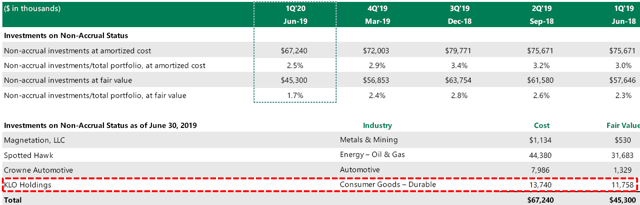

Spotted Hawk was marked down by an additional $7.7 million and impacted NAV per share by around $0.11. Total non-accruals currently account for 1.7% of total investments at fair value (previously 2.4%) and 2.5% of total investments at cost (previously 2.9%). If these investments were completely written off, it would impact NAV by around $0.67 or 3.5%.

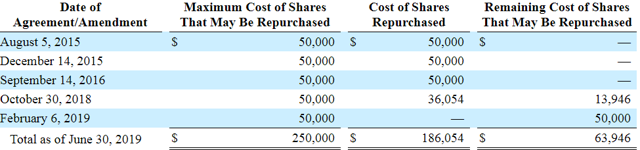

On February 6, 2019, the Board approved a new stock repurchase plan to acquire up to $50 million of the common stock. The new plan was in addition to the existing share repurchase authorization, of which $13.9 million of repurchase capacity remains. Since the inception of the share repurchase program, AINV has repurchased over 11 million shares at a weighted average price per share of $16.92 for a total cost of almost $188 million.

“We consider stock buybacks below NAV to be component of our plan to deliver value to our shareholders. We typically repurchase shares during both open window periods and we generally allocate a portion of our authorization to a 10b5-1 plan, which allows us to repurchase stock during blackout periods. Since the end of the quarter, we had continued to repurchase stock. We intend to continue to repurchase our stocks should it continue to trade at a meaningful discount to NAV.”

Since the end of the quarter, AINV has continued to repurchase stock (another 136,010 shares) with approximately $64 million available for stock repurchases (as of June 30, 2019) under its repurchase programs inclusive of the newly authorized $50 million plan:

As mentioned in previous reports, the company is in the process of repositioning the portfolio into safer assets including reducing its exposure to oil & gas, unsecured debt, and CLOs. The “core strategies” portion of the portfolio now accounts for 83% of all investments:

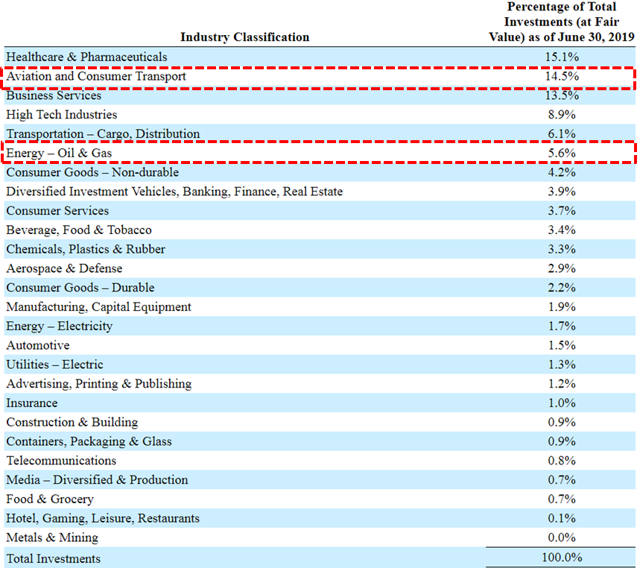

Its aircraft leasing through Merx Aviation remains the largest investment but is now below 15% of the portfolio and continues to pay dividend income. As mentioned in previous reports, AINV has been reducing its concentration risk including reducing its exposure to Merx. Energy, oil and gas investments account for around 5.6% of the portfolio:

This information was previously made available to subscribers of Premium BDC Reports, along with:

- AINV target prices and buying points

- AINV risk profile, potential credit issues, and overall rankings

- AINV dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.