The following is from the SUNS Update that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

SUNS Update Summary:

- NAV per share decreased by 0.2% and there was around $7 million or $0.43 per share in realized losses during the quarter related to exiting the previously discussed non-accrual investment in Trident USA Health Services.

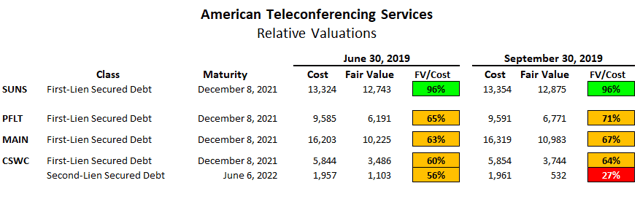

- I was expecting a decline in NAV per share related to American Teleconferencing Services being relatively overvalued compared to other BDCs unless there were positive developments with this investment during the recent quarter.

- However, SUNS did not markdown ATS and the other BDCs still have discounted values implying that there is still downside associated with this investment.

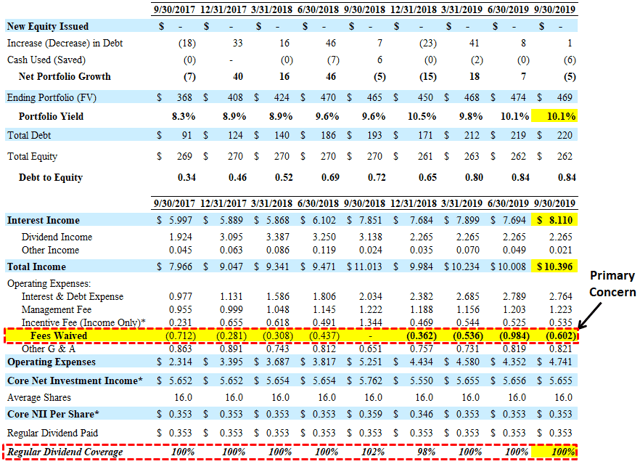

- SUNS hit its base-case projections covering its dividend only due to continued fee waivers. My primary concern is the continued reliance on fee waivers needed to cover its dividend implying that there could be longer-term dividend coverage issues.

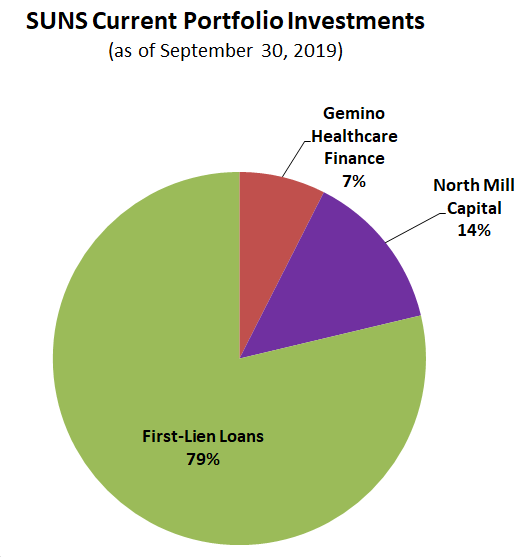

- However, there will likely be higher returns over the coming quarters from its equity investment in North Mill Capital that previously acquired the $40 million portfolio of Summit Financial Resources.

- SUNS remains underleveraged with plenty of growth capital and debt-to-equity of 0.84 compared to its target a range of 1.25 to 1.50.

Solar Senior Capital (SUNS) net asset value (“NAV”) per share decreased by 0.2% or $0.03 (form $16.34 to $16.31) and there was around $7 million or $0.43 per share in realized losses during the quarter related to exiting the previously discussed non-accrual investment in Trident USA Health Services. However, NAV per share was not impacted due to mostly being written off during the previous quarter. As mentioned in the previous report, I was expecting a decline in NAV per share related to American Teleconferencing Services being relatively overvalued compared to other BDCs “unless there were positive developments with this investment during the recent quarter”. SUNS did not markdown ATS during Q3 and the other BDCs still have the same discounts for their ATS investments as shown in the following table. CSWC marked a portion lower so there is clearly some downside coming for SUNS NAV and is likely not priced into the stock yet. PFLT has not released its SEC filings for calendar Q3 2019, and this investment will likely be discussed on the upcoming earnings call.

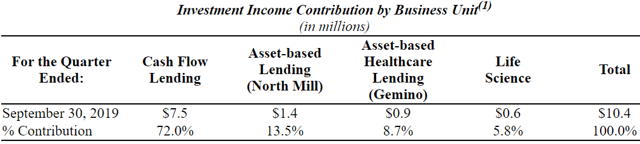

SUNS hit its base-case projections covering its dividend only due to continued fee waivers. My primary concern is the continued reliance on fee waivers needed to cover its dividend over the last four quarters (see details below) implying that there could be longer-term dividend coverage issues. However, there will likely be higher returns over the coming quarters from its equity investment in North Mill Capital (“NMC”) that previously acquired the $40 million portfolio of Summit Financial Resources:

“The Company continued its solid operating performance during the third quarter of 2019 with strong fundamentals of our portfolio companies and at 9/30/2019, 100% of the portfolio is performing. While it is early in the integration of North Mill Capital’s acquisition of Summit Financial Resources last quarter, we are encouraged by the broader geographic coverage and expanded pipeline of attractive investment opportunities across the platform. We continue to actively seek acquisitions to further build our asset-based lending capabilities. SUNS has ample capital to expand our specialty finance platform while continuing to be highly selective in cash flow lending.”

Its equity investment in NMC remains around 14% of the total portfolio but the weighted average yield from NMC increased from 13.5% to 14.2%.

SUNS remains a component in the ‘Risk Averse’ portfolio due to “true first-lien” positions, historically stable net asset value (“NAV”) and low non-accruals. Management has a history of doing the right thing including waiving fees to cover the dividend without the need to “reach for yield” and deploying capital in a prudent manner. The Board declared a monthly distribution for November of $0.1175 per share payable on December 3, 2019.

SUNS Liquidity and Capital Resources

As mentioned in previous reports, shareholders approved the reduced asset coverage ratio allowing for higher leverage and the immediate integration of its First Lien Loan Program (“FLLP”). SUNS will target a range of 1.25 to 1.50 debt-to-equity and took on additional debt associated with the FLLP but its debt-to-equity is still only 0.84.

Previously, SUNS announced that it had amended its credit facilities’ leverage covenants to allow for the asset coverage ratio minimum of 150%. As of September 30, 2019, SUNS had over $75 million of unused borrowing capacity under its revolving credit facilities. However, including NMC and Gemino non-recourse credit facilities, the company had approximately $155 million of unused borrowing capacity under its revolving credit facilities.

This information was previously made available to subscribers of Premium BDC Reports, along with:

- SUNS target prices and buying points

- SUNS risk profile, potential credit issues, and overall rankings

- SUNS dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.