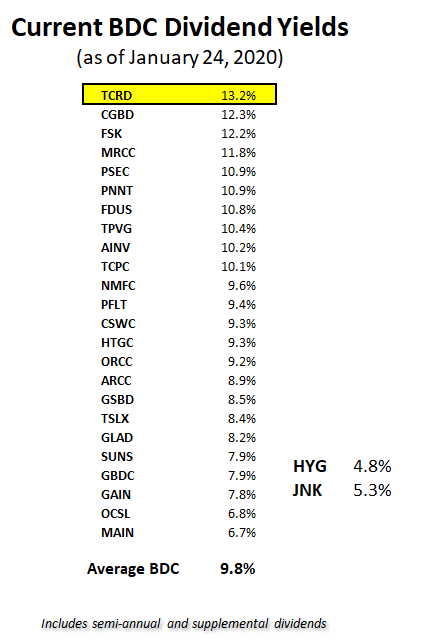

The following is from the TCRD Deep Dive that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

TCRD Dividend Coverage & Risk Profile Update

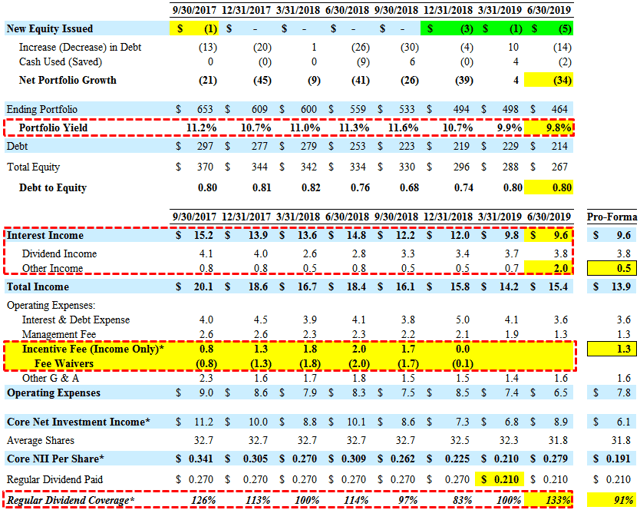

For Q3 2019, THL Credit (TCRD) hit its base-case projections with lower-than-expected portfolio growth offset by higher-than-expected portfolio yield covering its dividend by 106% due to continued fee waivers. It should be noted that if the company paid the full incentive fee, the dividend would not have been fully covered as shown in the ‘Pro-Forma’ column below. However, management will likely continue to waive fees as it grows the portfolio using higher leverage and rotating out of non-income producing assets to fully cover the dividend.

“We’re not anticipating taking an incentive fee given the losses that we’ve incurred during the portfolio for the remainder of 2020. So we think the dividend itself is sized accordingly and is okay. To the extent, the portfolio itself has been diversified enough to enable us to add more leverage, I think, the leverage that we put on the system would enable us to potentially earn an incentive fee in the future and still cover the dividend.”

On June 14, 2019, shareholders approved increased leverage and management intends to use partially to repurchase shares as well as grow and diversify the portfolio:

“Since our shareholders approved the reduced asset coverage requirement earlier this year, we have the ability to take on increased leverage. Our plan is to target modest leverage levels of 1.05 to 1.15 range in 2020 subject to successfully amending our credit facility. This will allow us to continue to diversify and grow the portfolio.”

—————–

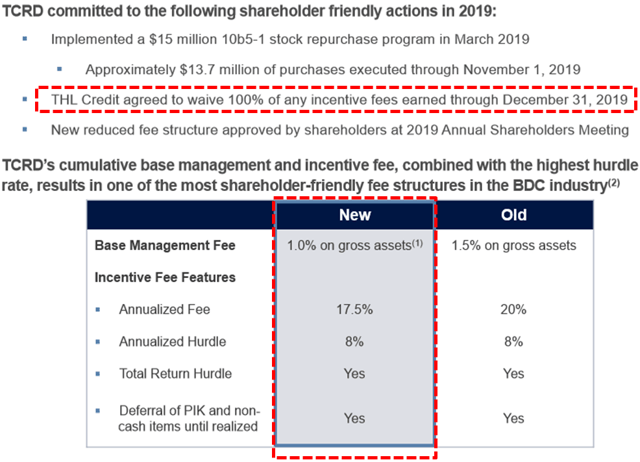

TRCD previously implemented a $15 million 10b5-1 stock repurchase plan and has been repurchasing shares “at levels that are accretive to shareholders with proceeds from exits of additional control equity positions this year”. During Q3 2019, the company repurchased 0.8 million shares at an average price of $6.70 (21% discount to previous NAV). The company continues to repurchase shares especially given that the stock is now trading 24% below NAV/book value:

“Since we initiated this plan in March 2019, we have repurchased $13.7 million of our stock or 91% of the target plan at a substantial discount to NAV. Repurchases in Q3 were accretive to book value by $0.05 per share. At the current repurchase plan in place, we expect to hit the $15 million amount by the end of the next month at which point we will reevaluate a new plan.”

“As there is still a dislocation between our book value and our stock price we’ll continue to aggressively buyback stock and accrete that to our shareholders as a good use of capital. The proceeds from Copperweld, one of our most concentrated positions at over 7% of the portfolio as of June can now be deployed across several new investments was to improve the overall diversity of the portfolio and may also be used for additional share buybacks under our $15 million 10b5-1 Stock Repurchase Plan.”

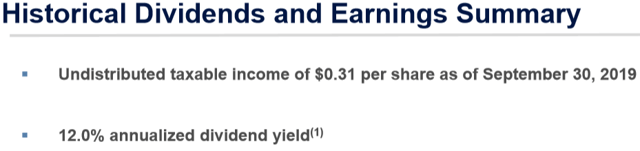

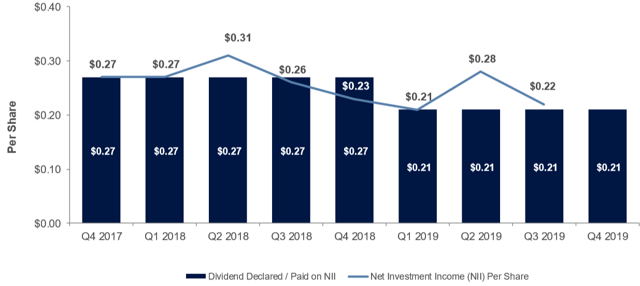

Undistributed taxable income increased from $0.29 per share to $0.31 per share.

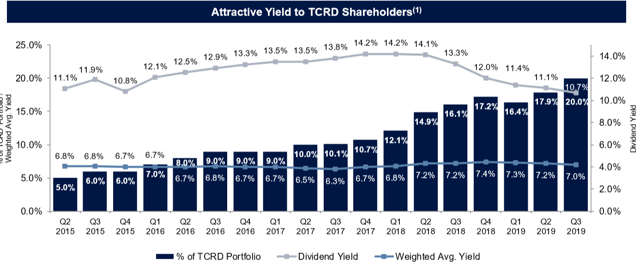

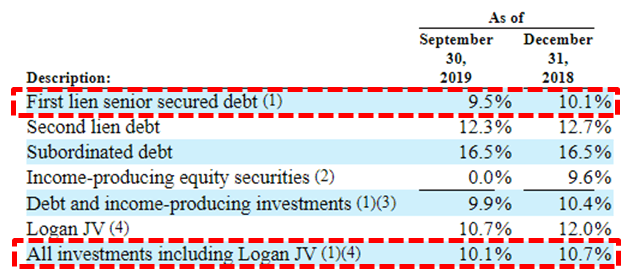

The company continues to ramp its THL Credit Logan JV from $257 million as of December 31, 2017, to $352 million as of September 30, 2019. However, the yield recently declined from 14.1% to 10.7% as shown in the following chart:

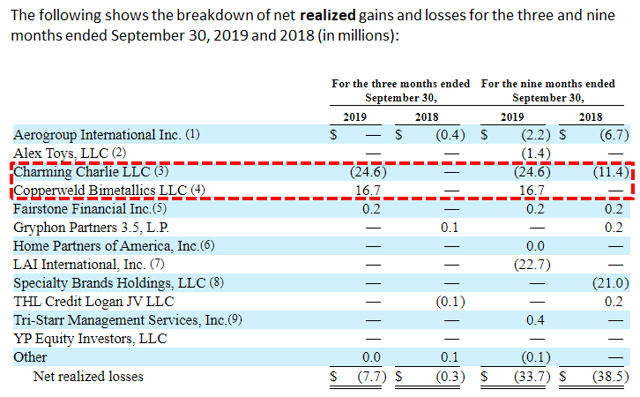

TCRD’s net asset value (“NAV”) per share has declined by almost 30% over the last three years due to having previous investments in higher-risk assets that underperformed. During Q3 2019, its NAV per share declined by another $0.15 or 1.8% (from $8.49 to $8.34) due to net realized/unrealized depreciation of $6.6 million or $0.21 per share. TCRD recognized realized losses of $7.7 million, mostly related to a realized loss of $24.6 million in connection with the liquidation of Charming Charlie, offset by a realized gain of $16.7 million from its investment in Copperweld Bimetallics LLC.

Most of the unrealized depreciation was due to a write-down of Holland Intermediate Acquisition Corp. and Logan JV, offset by reversals from Charming Charlie and Copperweld Bimetallics.

“Holland is a first lien investment and one of our three remaining energy credits. The business continued to face market headwinds this quarter due to overall reduced M&A activity in the energy space and was marked down accordingly. We’re very pleased with the results of our Copperweld exit this quarter. Copperweld is one of our control equity positions was originally an unsponsored deal that we took through and restructured in 2016. With managerial changes and the retention of an advisor, operations were stabilized and EBITDA grew, positioning the company for a sale. Cash proceeds received in dollars escrow totaled $35 million which were 1.6 times our original investment and a $1.5 million mark up from June 30. The total return on this investment, including interest and dividends was 3.2 times our original investment.”

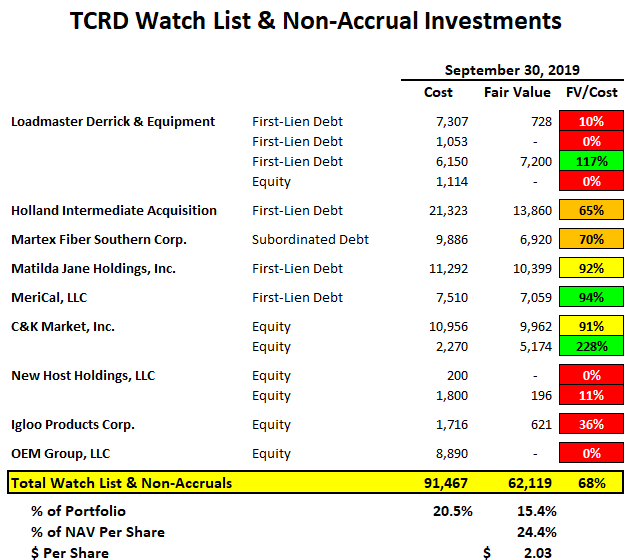

It should be noted that TCRD is considered higher-risk as shown in the BDC Risk Profiles report and has a larger amount of investments that are considered ‘watch list’ currently over 15% of the portfolio fair value (similar to MRCC and PNNT) implying that there will likely be additional NAV declines.

Over the last two quarters, non-accruals have decreased from 12.4% to 3.2% of the portfolio at cost but remain around 2.0% at fair value due to Loadmaster Derrick & Equipment that remains on non-accrual status.

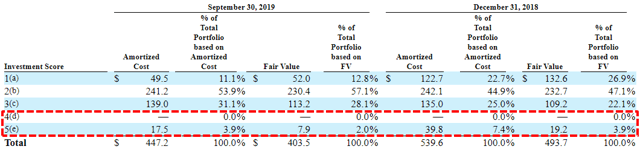

4 – The portfolio investment is performing materially below our underwriting expectations and returns on our investment are likely to be impaired. Principal or interest payments may be past due, however, full recovery of principal and interest payments are expected.

5 – The portfolio investment is performing substantially below expectations and the risk of the investment has increased substantially. The company is in payment default and the principal and interest payments are not expected to be repaid in full.

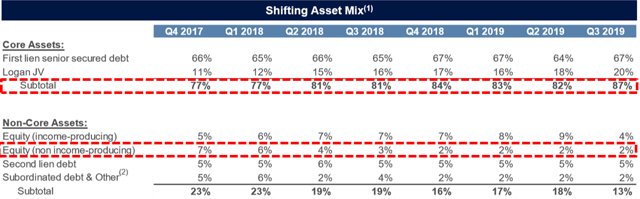

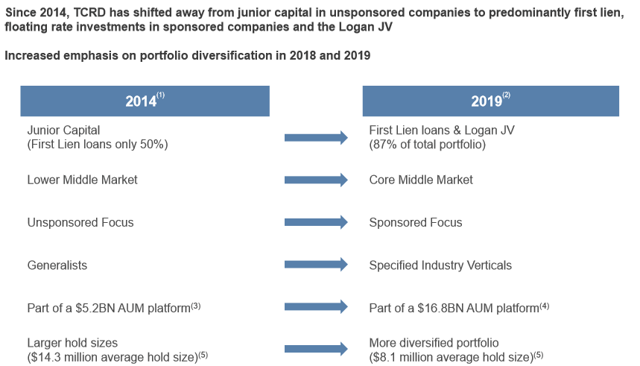

The company has been working to re-positioning its portfolio, including reducing the amount of non-income producing equity investments to 2% of the portfolio and 87% invested into Core Assets (first-lien debt and Logan JV) with a stated goal of 90%.

Christopher Flynn, CEO: “Over the past year, we have made significant progress on our strategic objectives across four dimensions— shifting the composition of our portfolio into primarily first lien floating rate assets, reducing our concentrated positions, increasing our investment in the Logan JV, and exiting our non-income producing securities. We remain confident that the steps we are taking to reduce risk in our portfolio will result in a more diversified senior secured floating rate portfolio that is positioned to deliver more stable and predictable returns for our shareholders over the long term.”

—————–

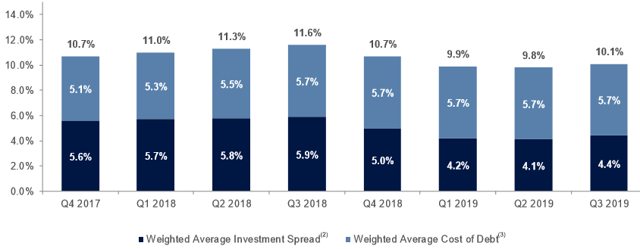

However, this has resulted in lower overall portfolio yield as shown below:

As mentioned in the previous report, the Advisor decided to waive additional incentive fees through the end of 2019, as well as to lower the base management fee to “more closely align with what it believes is appropriate for a first lien floating rate portfolio”. I believe that the new fee structure is very shareholder-friendly for the following reasons:

- Annual hurdle remains 8% (this is important as discussed in other reports)

- Total return hurdle remains (also important and best-of-breed)

- Base management fee reduced from 1.5% to 1.0% (this is among the lowest)

- Incentive fee reduced from 20.0% to 17.5%

- Deferral of PIK and non-cash items until realized

This information was previously made available to subscribers of Premium BDC Reports, along with:

- TCRD target prices and buying points

- TCRD risk profile, potential credit issues, and overall rankings

- TCRD dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.