The following information is from the MRCC Projections Update that was previously provided to subscribers of Premium BDC Reports along with target prices, dividend coverage and risk profile rankings, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all Business Development Companies (“BDCs”).

Quick Update:

As mentioned in “8% To 10% Balanced Portfolio Yield Investing In America: Part 2” on Seeking Alpha, I will be using this blog for additional public updates on individual BDCs.

Quick BDC Market Update

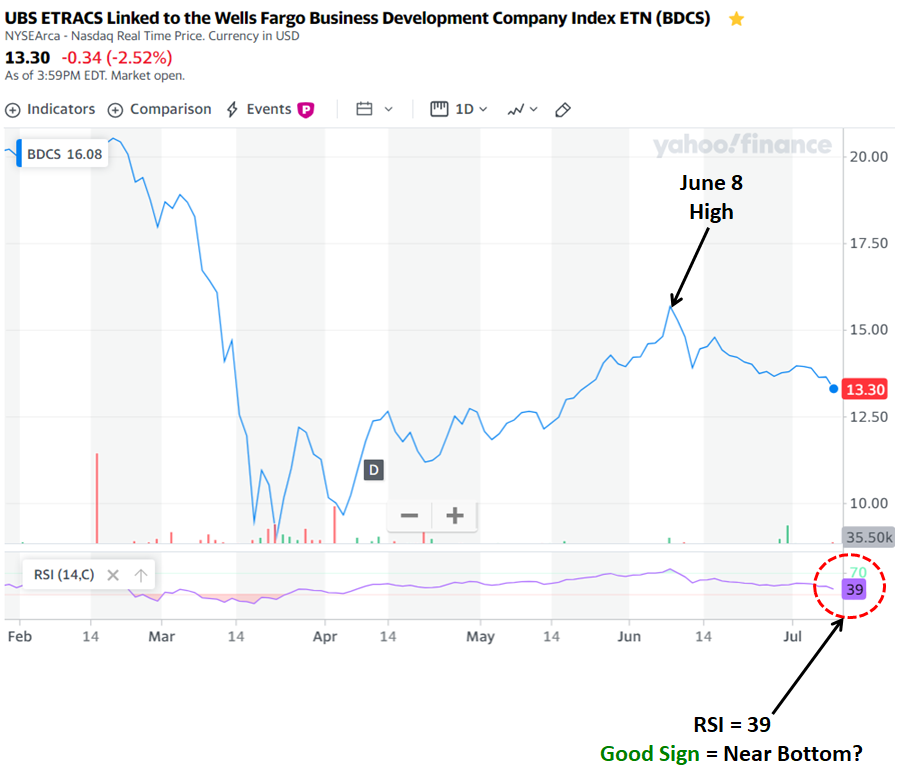

As mentioned in previous articles, I was expecting Business Development Company (“BDC”) pricing to pull back from the recent highs for various reasons including profit-taking and a partial return to “risk-off” mode. Please note that most BDC charts look similar to the one below with a peak on June 8 and then mostly down.

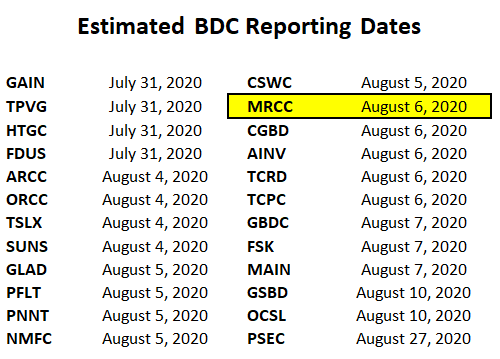

I am expecting volatility through July until BDCs start to report Q2 2020 results (see dates at the end). However, I am expecting many BDCs to report stronger-than-expected results including net asset value “NAV” increases, adequate dividend coverage, and reaffirming current dividends. Many of the NAV increases will be due to:

- Tightening of yield spreads (will impact each BDC differently depending on loan mix)

- Likely improved valuations related to COVID-19 as many BDCs made large general write-downs due to the uncertainty of the impact as of March 31

- PPP aid which reduced liquidity and leverage issues for many portfolio companies

It is important to understand that the values BDC management applied to their assets on March 31, 2020, were conservative as we did understand which companies/sectors would be the most impacted. Of course, there will be some increased non-accruals but for most BDCs, this will more than offset by improved valuations on other investments. As these results are reported (mostly in early August), it will drive some positive headlines and another rally in BDC pricing as investors are looking to improve portfolio yield/returns in this low yield environment.

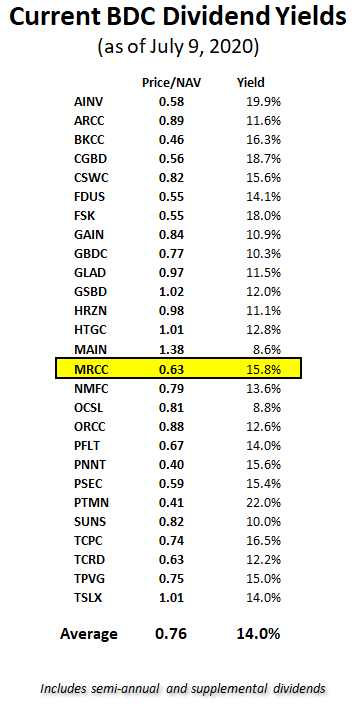

Clearly, the potential for additional or renewed lockdowns related to COVID-19 is a concern driving markets lower, including BDCs that are now yielding around 14% (see list below).

This article discusses Monroe Capital (MRCC) that is trading at a 37% discount to book value/NAV for the reasons discussed in “Why Investors Are Selling 12% Yielding Monroe Capital” that also predicted the recent dividend cut almost 6 months ago:

From January 26, 2020: “the quarterly dividend will likely be reduced to between $0.25 and $0.30. This also is shown in the worst-case projections that take into account continued credit issues likely from the investments discussed later in this report”

Issuing Shares Below NAV:

I am often asked about concerns that most BDCs have the ability to issue shares below NAV and hopefully, the following will help.

Most BDCs have the ability to issue shares below NAV typically related to lending facility covenants and/or extreme worst and best-case scenarios. During market volatility, BDCs could temporarily break a bank covenant and be forced to stop paying dividends until the company is back in compliance. The ability to issue even small amounts of equity can easily bring the BDC back into compliance. Also, having this option likely improves lending rates or other terms. I only invest in BDCs with higher quality management that would not issue shares below NAV unless it was an extreme case that could be either bad or good (opportunistic) such as using to make an acquisition at extremely low prices as ARCC did with Allied Capital and was a huge win for investors and NAV down the road:

The Company has also received stockholder approval to issue shares of its common stock under NAV for each of the last eight years (the “Annual Under NAV Approval”), and despite the Company trading below NAV for periods during such time frame, including for most of 2016, it has only used the flexibility provided by the Annual Under NAV Approval one time. In 2009, during a period of significant credit market volatility when credit spreads increased materially, the Company, acting pursuant to the Annual Under NAV Approval, prudently issued shares of its common stock at a price below NAV and invested the proceeds from such issuance at attractive returns to stockholders. These proceeds were also used to create liquidity and financial flexibility in an uncertain time of extreme volatility. While such issuance was at a price below NAV, it resulted in less than a 2.5% dilution in the aggregate net asset value of the Company. Additionally, the Company believes that this financial flexibility was a key component of the Company’s ability to opportunistically acquire Allied Capital Corporation, which transaction was agreed to on October 26, 2009 and closed on April 1, 2010 (the “Allied Acquisition”). The Company’s NAV increased during the one-year period following the date of the Company’s most recently determined NAV prior to such issuance, increasing from $11.21 (as of June 30, 2009) to $14.11 (as of June 30, 2010). The increase in the Company’s NAV from June 30, 2009 to June 30, 2010 includes a $1.11 per share increase related to the gain on the Allied Acquisition. Furthermore, for the one-year period following the date of such issuance, the Company’s total stockholder return outperformed that of every other BDC with a market capitalization of greater than $500 million. Therefore, periods of market volatility and dislocation have created, and may create again, favorable opportunities for the Company to make investments at attractive risk-adjusted returns, including opportunities that may increase NAV over the longer term, even if financed with the issuance of common stock below NAV.

Source: ARCC SEC Filing

MRCC is overleveraged and currently issuing shares through its “at the market” equity program at prices 30% to 40% below book value/NAV and will have a negative impact on upcoming results including NAV per share.

The following information was included in a recent SEC filing:

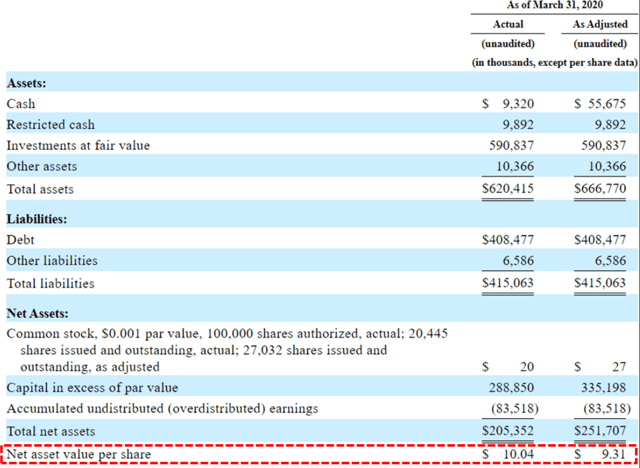

“this prospectus supplement and the accompanying prospectus. The equity distribution agreements provide that we may offer and sell up to $50,000,000 of our common stock from time to time through the Sales Agents in negotiated transactions or transactions that are deemed to be “at the market offerings,” as defined in Rule 415 under the Securities Act of 1933, as amended. As of the date of this prospectus supplement, we have sold $8.7 million of our common stock under the equity distribution agreements. Our common stock is listed on The Nasdaq Global Select Market under the symbol “MRCC.” On June 23, 2020, the last reported sale price of our stock on The Nasdaq Global Select Market was $7.12 per share. Our net asset value as of March 31, 2020 was $10.04 per share.”

“The table below assumes that we will sell all of the remaining common stock available under the program as of June 23, 2020 of $41.3 million at a price of $7.12 per share (the last reported sale price of our common stock on The Nasdaq Global Select Market on June 23, 2020)…The following table sets forth our capitalization as of March 31, 2020, and on an as adjusted basis giving effect to the $6.2 million of common stock sold from March 31, 2020 to June 23, 2020 at an average price of $7.86 per share and to the assumed sale of $41.3 million of our common stock at a price of $7.12 per share (the last reported sale price of our common stock on The Nasdaq Global Select Market on June 23, 2020) less commissions and expenses.”

It should be noted that as of the writing of this article, the stock was trading at $6.33 (not $7.12) which is a 37% discount to NAV and would have a larger impact if the company is actively issuing shares. Please keep in mind that any shares issued after June 30, 2020, will impact Q3 2020 results (not Q2 2020).

Source: MRCC SEC Filing

Previous Insider Purchases & Ownership:

- It should be noted that the most recent insider purchases were at prices below $7.00:

Source: Gurufocus

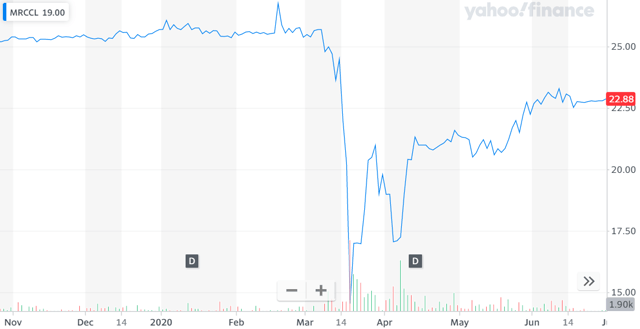

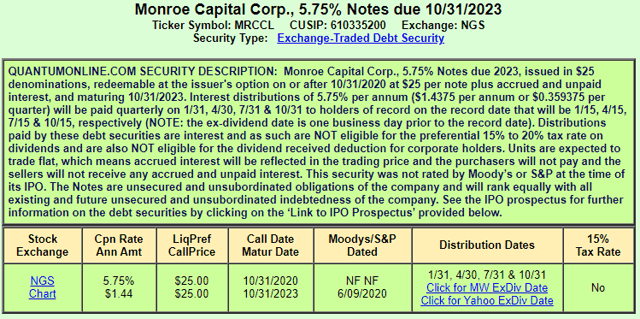

Monroe Capital 5.75% Notes (MRCCL) due 10/31/2023:

I have previously invested in MRCC’s Baby Bond “MRCCL” but sold due to the amount of leverage, lower-quality assets, and declining interest expense coverage all of which increase its risk ranking. As mentioned in previous articles, I rank each Baby Bond using portfolio credit quality and many metrics including the ones listed below.

Please see the following links from Investopedia for more information:

MRCC Dividend Update

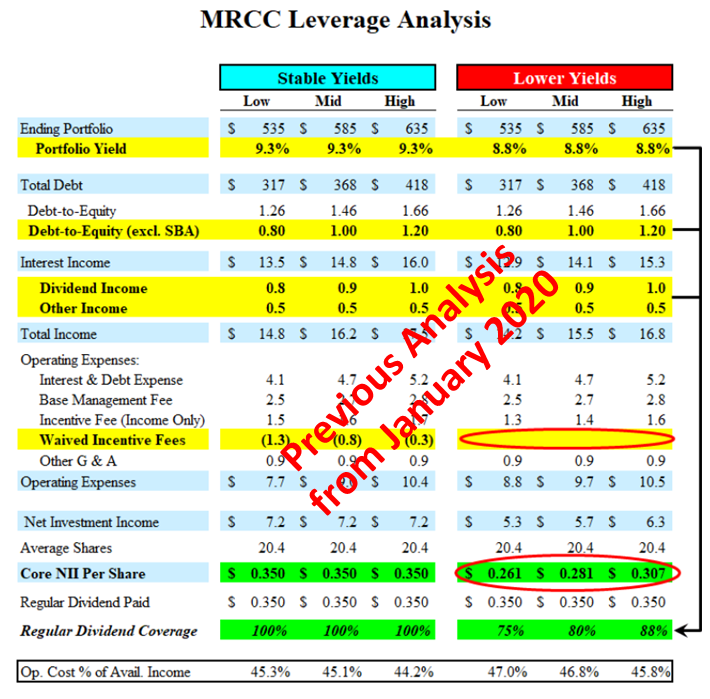

One of the methods that I use to assess BDC dividend coverage is my Optimal Leverage Analysis based on portfolio growth using available cash and borrowings (leverage) as well as changes in portfolio yield and potential credit issues. This is a longer-term run rate analysis of coverage that includes “stable” and “lower” portfolio yields with minimal amounts of non-recurring income and is an apples-to-apples comparison using similar amounts of leverage. In May 2020, MRCC announced a quarterly dividend reduction from $0.35/share to $0.25/share.

My Current BDC Investment Plan

My last two major purchases of multiple BDC common stocks were March 12 and March 19 and included 14 higher-quality BDCs. I was lucky and bought at or very near the previous lows and now collecting dividends and:

- Waiting for BDCs to report Q2 results (see dates below),

- Watching for preliminary result announcements (similar to NMFC discussed last week),

- Gathering information (portfolio and capital structure updates),

- Updating projected changes to NAV and dividend coverage for each BDC,

- Planning for future purchases.

Full BDC Reports:

This information was previously made available to subscribers of Premium BDC Reports, along with:

- MRCC target prices and buying points

- MRCC risk profile, potential credit issues, and overall rankings

- MRCC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.