The following information was previously provided to subscribers of BDC Buzz Premium Reports along with:

- ARCC target prices, buying points, and suggested limit orders (used during market volatility).

- ARCC risk profile, potential credit issues, changes in NAV, and overall rankings. Please see BDC Risk Profiles for additional details.

- ARCC dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

ARCC December 31, 2023, Quick Update

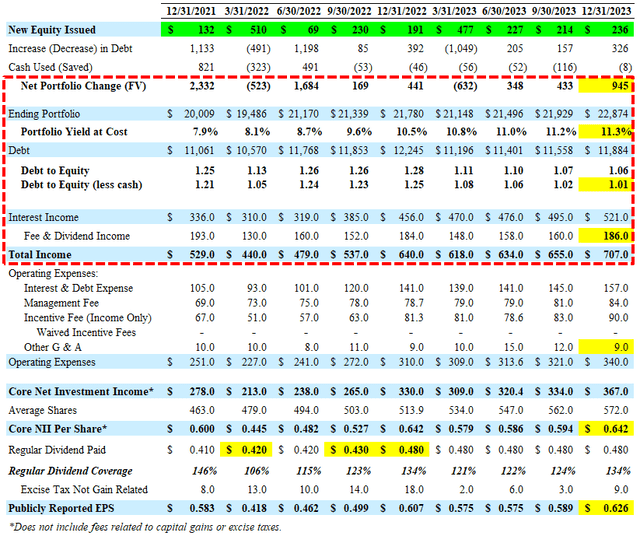

For Q4 2023, ARCC easily beat its best-case projections, mostly due to much higher-than-expected portfolio growth and continued higher amounts of dividend income (of $129 million), covering its regular dividend by 134% (excluding excise tax of $9 million). The company reaffirmed its regular dividend of $0.48 per share, as expected in the previous base case projections. The amount of payment-in-kind (“PIK”) interest income increased to 6.6% of total income with an average of around 6.4% for 2023. There was a slight decline in leverage with its debt-to-equity ratio declining from 1.02 to 1.01 (net of cash) due to the issuance of 12.0 million shares (accretive to NAV) through its “at the market” ATM equity program raising a total of $236 million in net proceeds.

Kipp deVeer, CEO: “Our record fourth quarter Core EPS and net asset value per share concluded another successful year for our company. We continue to drive strong credit and financial results using our extensive sourcing, underwriting and portfolio management capabilities. We believe we are heading into 2024 from a position of strength and will seek to build upon our 14-year track record of paying a stable regular quarterly dividend for our shareholders.”

It is important to point out that its regular dividend of $0.48 per share is adequately covered, especially given that the company has earned an average of almost $0.61 per share over the last five quarters. As mentioned in the weekly BDC sector updates, I am expecting fewer (and smaller) increases in the regular dividends, as BDCs prepare for potentially lower rates.

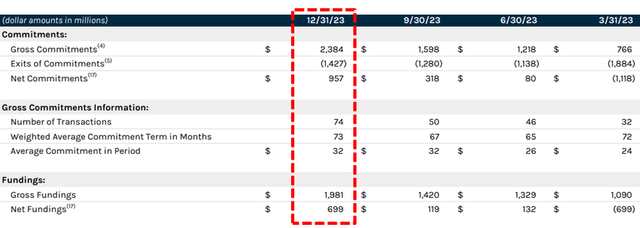

As expected, ARCC had a busy Q4 2023 with almost $2.4 billion of new commitments and almost $2.0 billion of total fundings. So far in Q1 2024, the company made new commitments of $705 million, of which $478 million were funded. However, there have already been $695 million of exits driving around $19 million or $0.03 per share of realized gains.

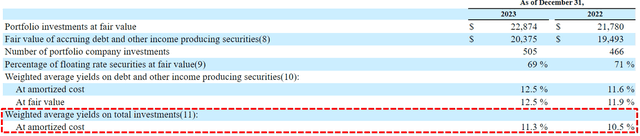

During Q4 2023, ARCC sold another $351 million of loans to IHAM that should continue to drive higher dividend income over the coming quarters and the overall portfolio yield has increased from 10.5% to 11.3% over the last four quarters:

In January 2024, the Board authorized an amendment to its existing $1.0 billion stock repurchase program to extend the expiration date from February 15, 2024 to February 15, 2025.

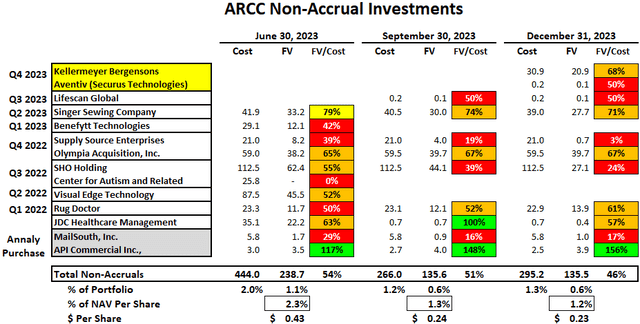

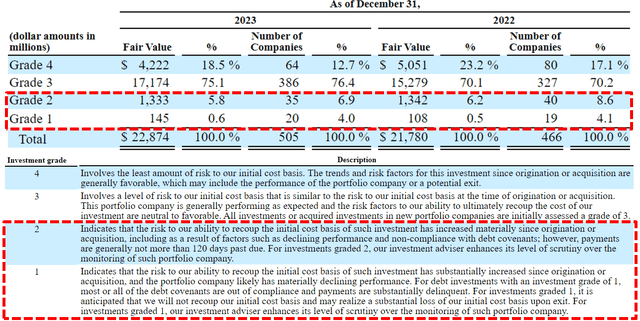

Non-accrual investments remain 0.6% of the total portfolio due to adding its watch list investment in Kellermeyer Bergensons (provider of janitorial and facilities management services) mostly offset by additional markdowns for Singer Sewing, SHO Holding (Shoes for Crews), and Supply Source Enterprises. Also, there was a very small position in Aventiv (Securus Technologies) added to non-accrual which is held by TCPC and PSEC. These investments have been discussed in previous reports and already included in ARCC’s watch list investments which will be discussed in the updated ARCC Deep Dive Projection report. Please note that ARCC has a very large portfolio with 505 portfolio companies valued at around $22 billion, so there will always be a certain amount of non-accruals.

There amount of higher-risk Grade 1 and Grade 2 credit-rated investments decreased slightly from 6.5% to 6.4% of the portfolio fair value and likely includes many of the previously discussed watch list investments. The weighted average grade of the portfolio at fair decreased from 3.2 to 3.1 (will also be discussed in the updated ARCC Deep Dive Projection report).

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy-to-digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning, we provide quick updates for the sector, including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on individual BDCs each week prioritized by focusing on buying opportunities and potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Weekly General Updates or Comparison Reports – A series of updates discussing ‘Building a BDC Portfolio’, suggested pricing and limit orders, expense/return ratios, interest rates, leverage, BDC Investment Grade Notes/Baby Bonds, portfolio mix, and potential impacts on dividend coverage and risk.

![]()