The following information was previously provided to subscribers of BDC Buzz Premium Reports along with:

- GBDC target prices, buying points, and suggested limit orders (used during market volatility).

- GBDC risk profile, potential credit issues, changes in NAV, and overall rankings. Please see BDC Risk Profiles for additional details.

- GBDC dividend coverage projections (base, best, worst-case scenarios). Please see BDC Dividend Coverage Levels for additional details.

![]()

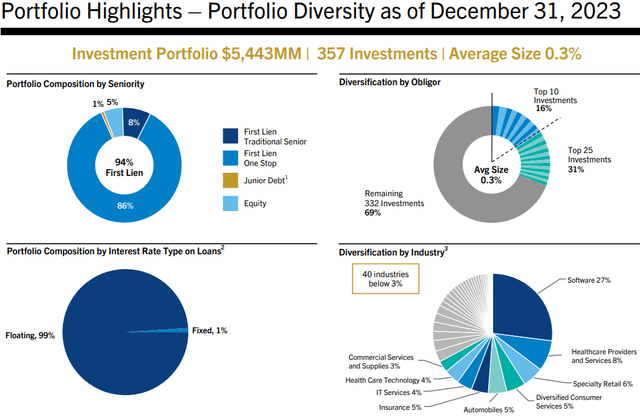

Golub Capital (GBDC) is considered a lower-risk BDC for many reasons, including its higher credit quality portfolio of mostly lower yield first-lien and one-stop loans with strong covenant and security protections in mostly non-cyclical sectors. The portfolio is lower-yielding 94% first-lien, highly diversified with very low concentration risk, an average investment size of 0.3% of the portfolio fair value, and the top 25 accounting for around 31%.

“GBDC’s portfolio remained highly diversified by obligor with an average investment size of approximately 30 basis points with 95% of our investment portfolio was comprised of first lien, senior secured floating rate loans and defensively positioned in what we believe to be resilient industries.”

GBDC Quick Quarterly Update (December 31, 2023)

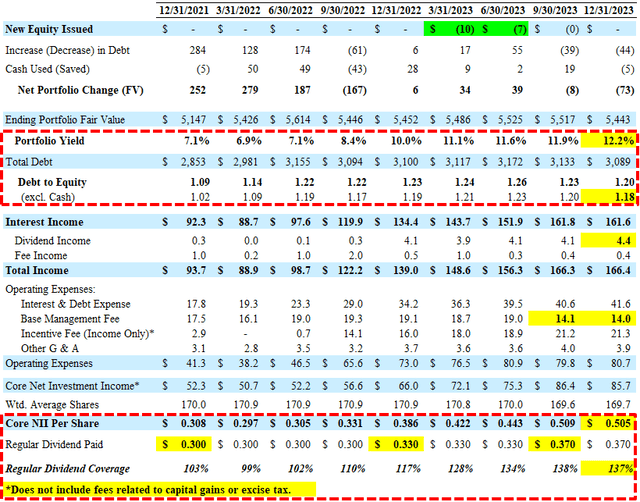

- Earnings: Reported between its base and best-case projections due to a higher-than-expected portfolio yield (increased from 11.9% to 12.2%) combined with higher dividend income and lower ‘Other G & A’. It should be noted that quarterly interest income has increased from $89 million to $162 million or 82%, increasing NII per share from $0.30 to almost $0.51 per share (excluding tax accrual) over the last 7 quarters.

- PIK Interest Income: Decreased from 8% (during the previous quarter) to 7% of total income but remains higher than previous levels (around 5% to 6%).

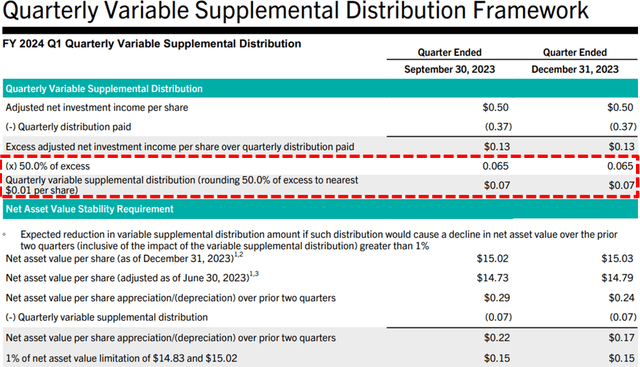

- Dividends: Recently its regular quarterly distribution from $0.37 to $0.39 per share plus a supplemental dividend of $0.07 per share for Q4 2023 (paid in Q1 2024), as expected in the previous best-case projections (shown below). Similar to other BDCs, GBDC has adopted a variable portion of its dividend policy to pay out the excess earnings as portfolio yields remain higher.

- Share Repurchases: None likely due to trading closer to NAV and maintaining leverage.

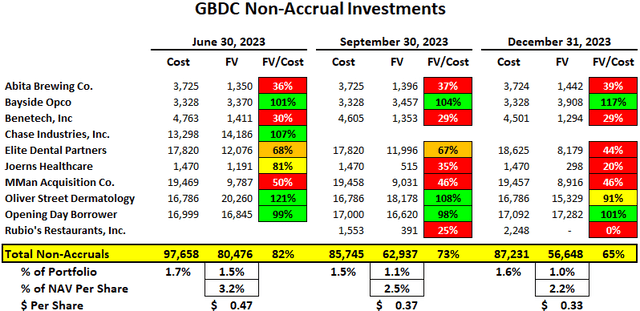

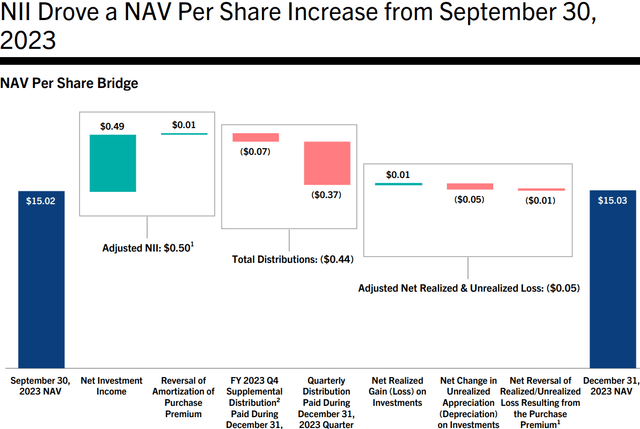

- NAV per Share: Increased by $0.01 (from $15.02 to $15.03) due to overearning the dividends (regular and supplemental) mostly offset by unrealized losses related to Oliver Street, Elite Dental, and Rubio’s Restaurants

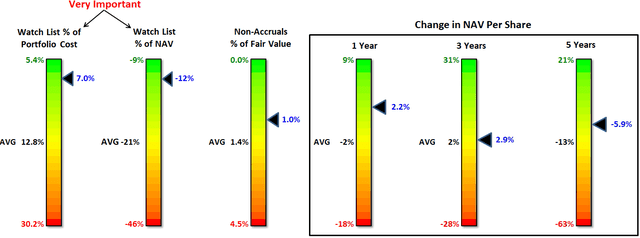

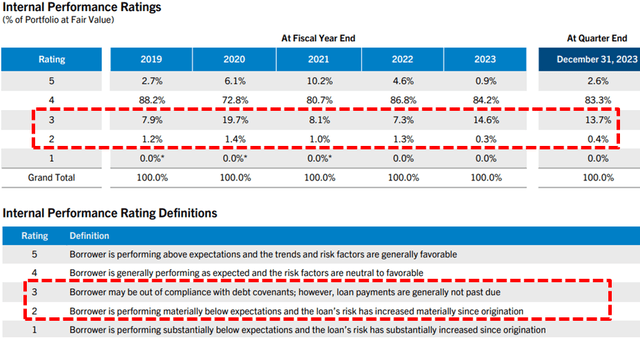

- Credit Quality: Non-accruals decreased from 1.1% to 1.0% of the portfolio fair value mostly due to marking down Oliver Street (dba U.S. Dermatology Partners) and Elite Dental as well as completely writing off Rubio’s Restaurants. However, Bayside and Opening Day remain fully valued implying likely temporary and could be added back to accrual. The amount of investments rated Category 2 and 3 decreased from 14.9% to 14.1% (implies improved portfolio credit quality).

- This information will be discussed in the updated GBDC Deep Dive Projection report.

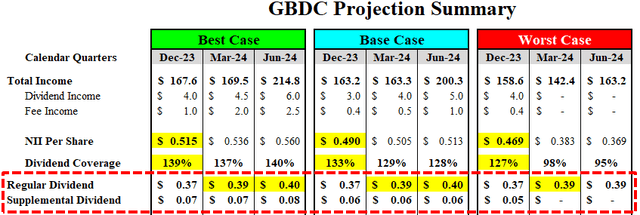

As shown below, I was expecting $0.07 per share of supplemental dividends in the best-case projections as well as additional supplemental dividends over the coming quarters partially supported by the lower fee structure:

Non-accruals decreased slightly from 1.1% to 1.0% of the portfolio fair value mostly due to marking down Oliver Street (dba U.S. Dermatology Partners) and Elite Dental as well as completely writing off Rubio’s Restaurants. This will be discussed in the updated GBDC Deep Dive report along with the other non-accruals. GBDC has around 357 portfolio company investments, so a certain amount on non-accrual status is to be expected.

GBDC maintains a credit watch list with portfolio companies placed into one of five categories, with Category 5 being the highest rating and Category 1 being the lowest. The amount of Category 2 and 3 decreased from 14.9% to 14.1%.

Changes to GBDC Fee Structure & Financial Analysis

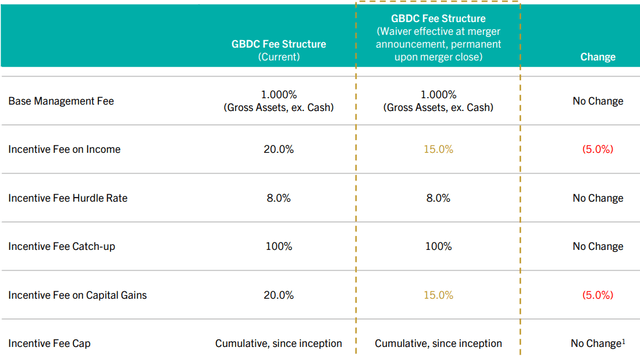

As mentioned later, GBDC’s investment adviser has agreed to reduce the income incentive fee and capital gain incentive fee rate from 20.0% to 15.0% effective as of January 1, 2024, and was taken into account with the previously updated projections. Also, in August 2023, GBDC announced the reduction of its base management fee from 1.375% to 1.000%.

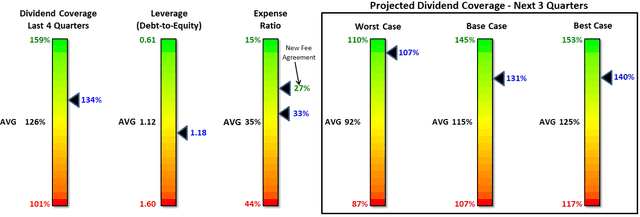

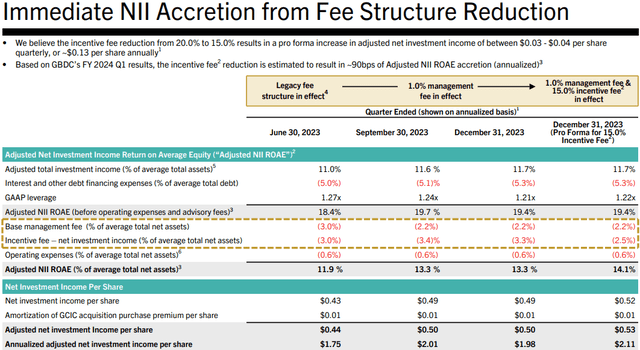

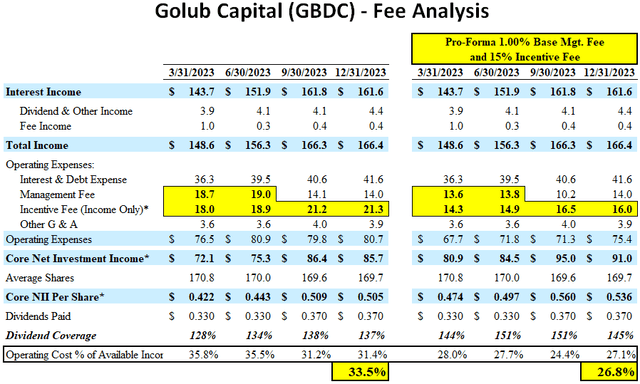

GBDC now has one of the best fee agreements in the sector with the lowest base management fee (similar to BXSL, GSBD, and PFLT) combined with the highest hurdle rate at 8.00%, and a cumulative ‘total return’ hurdle or ‘look back’ provision when calculating income incentive fees to protect shareholders from capital losses. I would like to see other BDCs join this group of lower fee structures that would encourage larger institutional investors to sector driving higher multiples and returns for current shareholders. After taking into account the reduced fees, GBDC’s expense ratio declines from 33.5% to 26.8% which is among the lowest in the sector, especially compared to other externally managed BDCs (as shown later).

The following table shows the pro-forma changes and impact to earnings and dividend coverage. Please note that the reduced base management fee was already included in calendar Q3 and Q4 2023 results so the change in pro-forma earnings was around $0.03 per share compared to $0.05 per share for the previous quarters. Basically, GBDC is able to pay at least $0.20 per share annually taking into account the reduced fees. Also, given the previous increases in portfolio yield and maintaining credit quality, the company can easily support dividends of $0.50 per share per quarter (or $2.00 annually) which is taken into account with the GBDC’s target prices.

What Can I Expect Each Week With a Paid Subscription?

Each week we provide a balance between easy-to-digest general information to make timely trading decisions supported by the detail in the Deep Dive Projection reports (for each BDC) for subscribers that are building larger BDC portfolios.

- Monday Morning Update – Before the markets open each Monday morning, we provide quick updates for the sector, including significant events for each BDC along with upcoming earnings, reporting, and ex-dividend dates. Also, we provide a list of the best-priced opportunities along with oversold/overbought conditions, and what to look for in the coming week.

- Deep Dive Projection Reports – Detailed reports on individual BDCs each week prioritized by focusing on buying opportunities and potential issues such as changes in portfolio credit quality and/or dividend coverage (usually related). This should help subscribers put together a shopping list ready for the next general market pullback.

- Weekly General Updates or Comparison Reports – A series of updates discussing ‘Building a BDC Portfolio’, suggested pricing and limit orders, expense/return ratios, interest rates, leverage, BDC Investment Grade Notes/Baby Bonds, portfolio mix, and potential impacts on dividend coverage and risk.

![]()