The following is from the TCPC Update that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

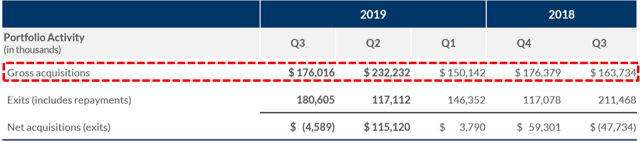

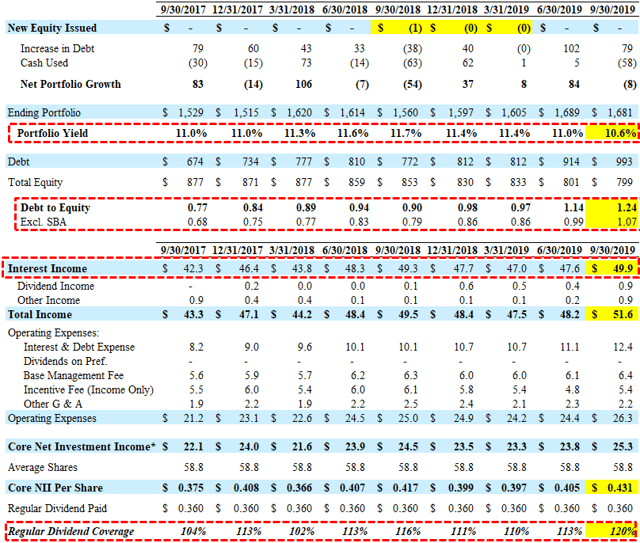

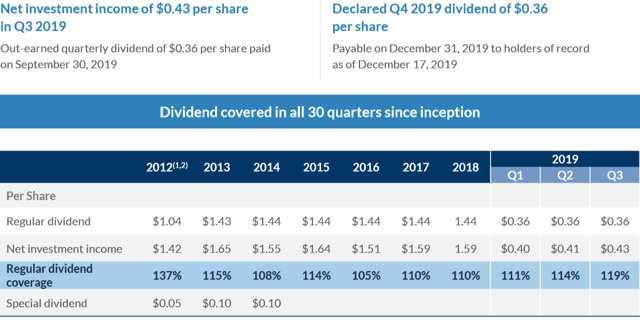

BlackRock TCP Capital (TCPC) beat its best case projections covering its dividend by 120% that included $0.06 per share of income related to prepayment premiums and accelerated original issue discount amortization. The company also reported strong originations:

—————–

Howard Levkowitz, TCPC Chairman and CEO: “We are pleased to have continued our record of covering our dividend for the 30th consecutive quarter, with a dividend coverage ratio of 119% in the third quarter. We also further expanded our diverse leverage program by completing a $150 million unsecured note issuance at an attractive interest rate of 3.9%., While our income reflected significant repayments, we were able to offset those repayments with another quarter of strong originations. We continue to have a solid pipeline of new investment opportunities and believe we are well-positioned to continue to deliver attractive risk-adjusted returns to our shareholders.”

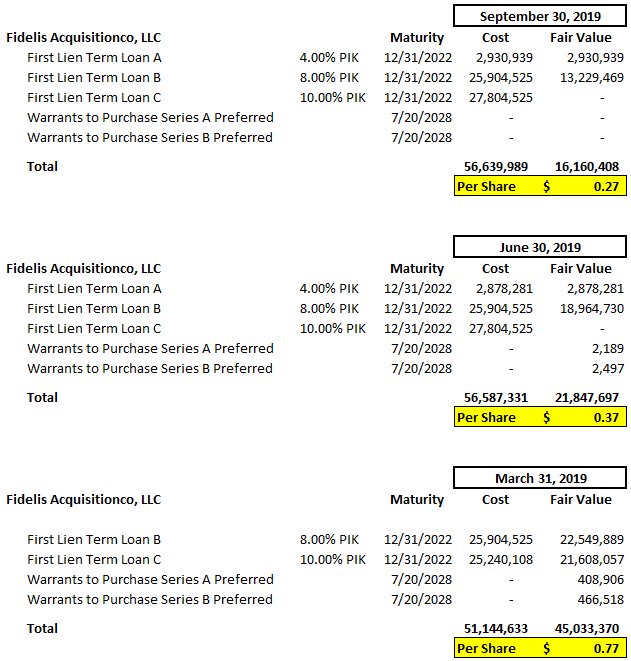

Its net asset value (“NAV”) per share declined slightly by $0.05 or 0.4% (from $13.64 to $13.59) mostly due to unrealized losses from previously discussed investments partially offset by overearning the dividend. Similar to the previous quarter, the largest markdown was its investment in Fidelis Acquisitions, LLC (“Fidelis”) that was added to non-accrual in Q2 2019 and marked down another $5.7 million during Q3 2019.

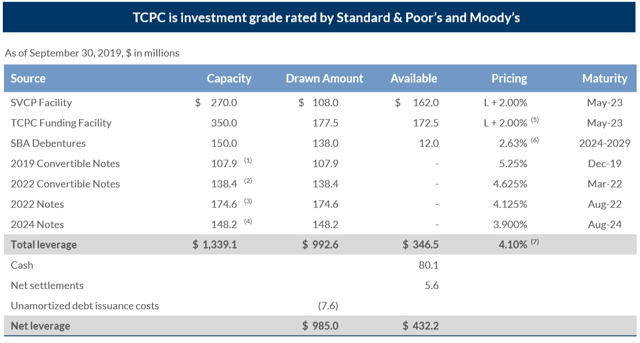

As of September 30, 2019, available liquidity was $432 million, including $347 million in available borrowing capacity and $80 million in cash and cash equivalents. On August 23, 2019, the company issued $150 million of unsecured 3.900% notes that mature on August 23, 2024. Also in August 2019, the company expanded the total capacity of its SVCP Facility by $50 million to $270 million. On November 7, 2018, Moody’s Investors Service initiated an investment grade rating of Baa3, with stable outlook. On November 8, 2018, S&P Global Ratings reaffirmed its investment-grade rating of BBB-, with negative outlook. Both ratings include consideration of the Company’s reduced asset coverage requirement.

The company consistently over-earns its dividend growing its undistributed taxable income plus roll-forward spillover that will hopefully be used for potential special dividends.

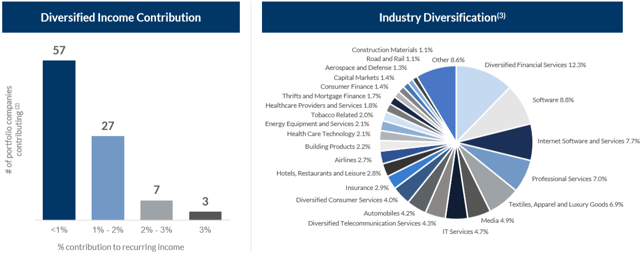

As shown below, TCPC’s portfolio is highly diversified by borrower and sector with only three portfolio companies that contribute 3% or more to dividend coverage:

On February 8, 2019, shareholders approved the reduced asset coverage ratio allowing higher leverage and reduced management fee to 1.00% on assets financed using leverage over 1.00 debt-to-equity, reduced incentive fees from 20.0% to 17.5% and hurdle rate from 8% to 7% as well as “continue to operate in a manner that will maintain its investment-grade rating”.

On August 6, 2019, the Board re-approved its stock repurchase plan to acquire up to $50 million of common stock at prices below NAV per share, “in accordance with the guidelines specified in Rule 10b-18 and Rule 10b5-1”. There is a good chance that the company will repurchase additional shares if the stock price declines below NAV again which is now $13.59 (reduced asset coverage ratio and higher leverage can be used for accretive stock repurchases).

This information was previously made available to subscribers of Premium BDC Reports, along with:

- TCPC target prices and buying points

- TCPC risk profile, potential credit issues, and overall rankings

- TCPC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.