The following is from the PFLT Update that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

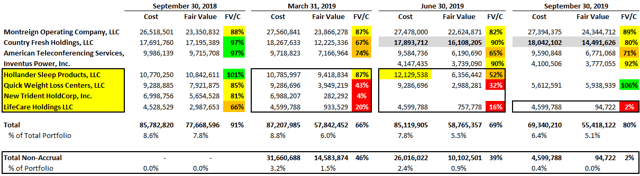

PennantPark Floating Rate Capital (PFLT) net asset value (“NAV”) per share declined by $0.10 or 0.8% (from $13.07 to $12.97) mostly due to the previously discussed investments including Country Fresh Holdings that is still not considered a ‘non-accrual’ but was restructured during the previous quarter. The following is from the PFLT update earlier this week:

“As discussed in the PFLT Deep Dive report, I am expecting the resolution for many of the recent credit issues and will be watching closely with the updated results. However, there is a good chance that its position in LifeCare Holdings LLC will be mostly written off due to a recent disclosure statement filed on November 15, 2019.”

As predicted, PFLT exited its non-accrual investment in Hollander Sleep Products and restructured its non-accrual investment in Quick Weight Loss Centers during the quarter. LifeCare Holdings remains the only investment currently on non-accrual status and was mostly written off during the recent quarter likely for the reasons discussed in the previous update. Non-accruals are now only 0.4% of the portfolio at cost and 0.0% at fair value with no further meaningful impacts to NAV per share. Also predicted in the previous report, its investment in Montreign Operating Company was marked up.

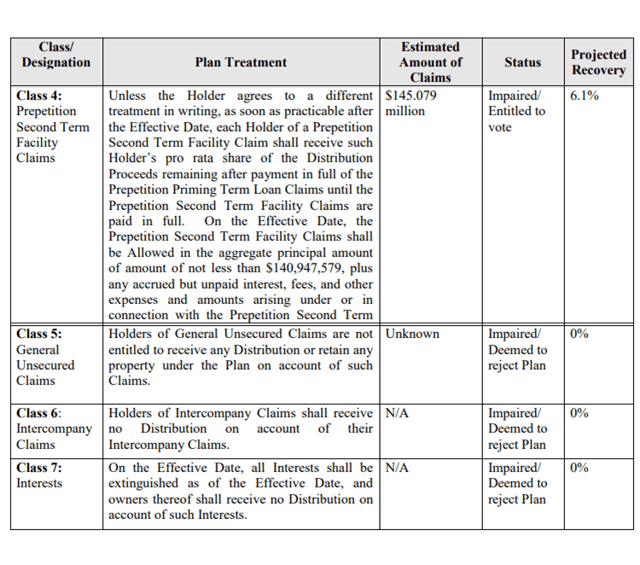

LifeCare Holdings is a bankrupt operator of senior care facilities filed a liquidation plan that would largely shut out creditors after selling off assets. There is a confirmation hearing set for January 14, 2020. However, it should be pointed out that this investment is already flagged as part of the ‘watch list’ in the previous Deep Dive report and is now mostly written off as of September 30, 2019, compared to the estimated 6% “projected recovery” discussed below:

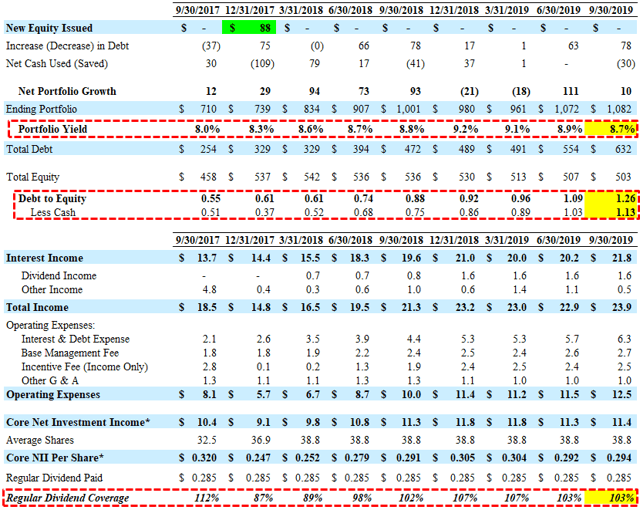

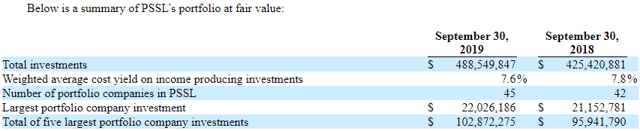

For calendar Q3 2019, PFLT reported just above its base case projections with continued higher use of leverage partially offset by lower portfolio yield. Dividend income from the PennantPark Senior Secured Loan Fund (“PSSL”) remained stable.

For the three months ended September 30, 2019, PFLT invested $141 million of in 6 new and 23 existing portfolio companies with a weighted average yield of 8.5% with sales and repayments of $127 million. As expected, the company continues to increase leverage with a debt-to-equity of 1.26 (1.13 excluding cash) utilizing its Board approved reduced asset coverage ratio, effective as of April 5, 2019.

Art Penn, Chairman and CEO. “We are pleased that our strategy and execution has resulted in net investment income covering our dividend. We believe that our earnings stream will continue to have a nice tailwind, creating value for our investors as we gradually increase our debt to equity ratio, while maintaining a prudent debt profile. Additionally, our overall portfolio continues to perform well. Our portfolio companies generally have strong underlying financial performance.”

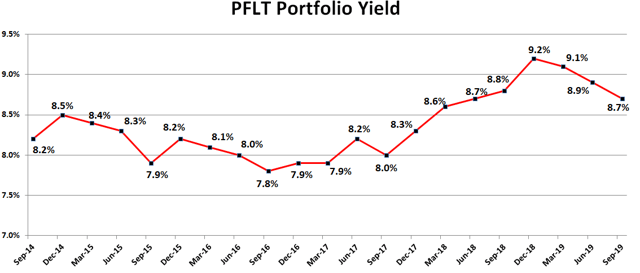

As discussed in previous reports, PFLT’s portfolio yield was increasing primarily due to rising LIBOR and additional returns from the PSSL.

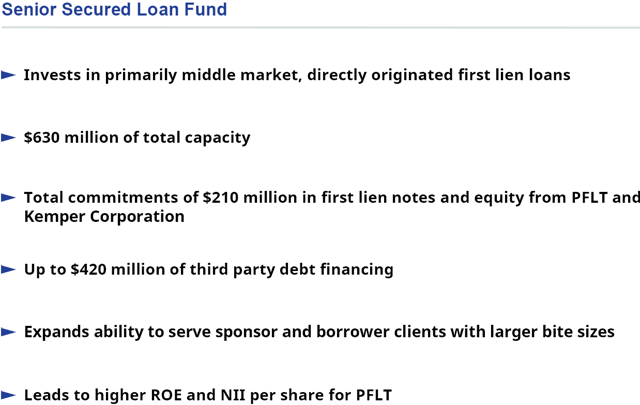

PFLT has grown its PSSL portfolio from $425 million to $489 million over the last four quarters but the weighted average yield on investments decreased from 7.8% to 7.6%:

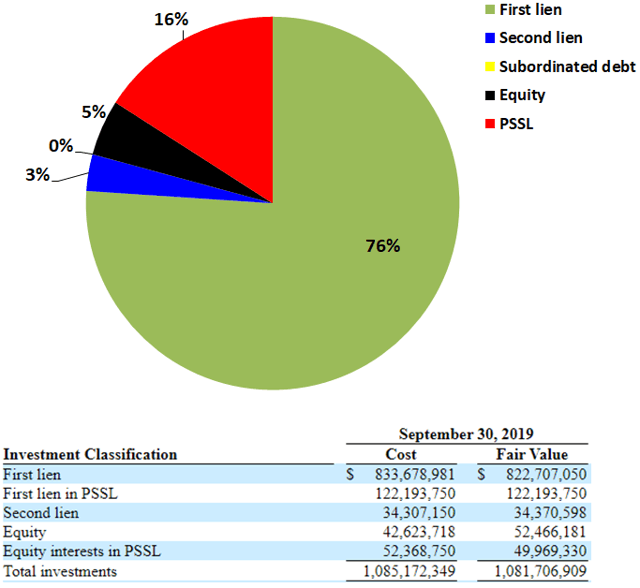

The portfolio remains predominantly invested in first-lien debt at around 76% portfolio and the PSSL has grown from 9% to 16% over the last five quarters. It is important to note that its PSSL is 100% invested in first-lien debt.

This information was previously made available to subscribers of Premium BDC Reports, along with:

- PFLT target prices and buying points

- PFLT risk profile, potential credit issues, and overall rankings

- PFLT dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.