The following is from the CGBD Deep Dive that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

CGBD Update Summary:

- The following is a preview for a Seeking Alpha article coming out early next week discussing the pros and cons of investing CGBD including conservative asset valuations/dividend philosophy, share repurchases, new management, and investor perceptions of recent credit issues likely driving its discounted stock price.

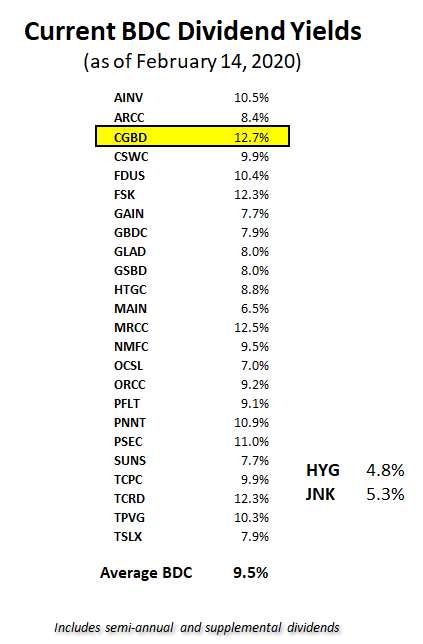

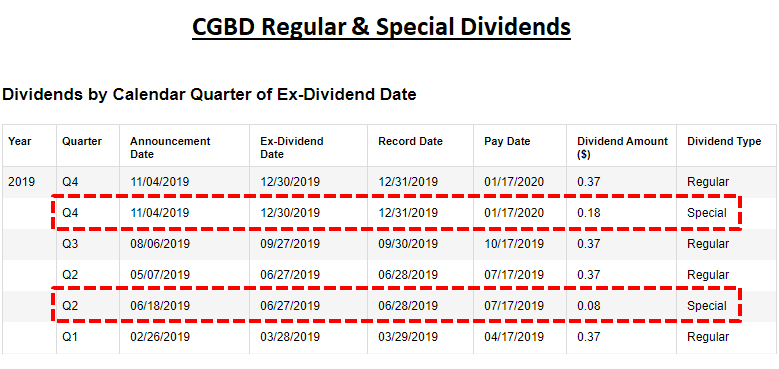

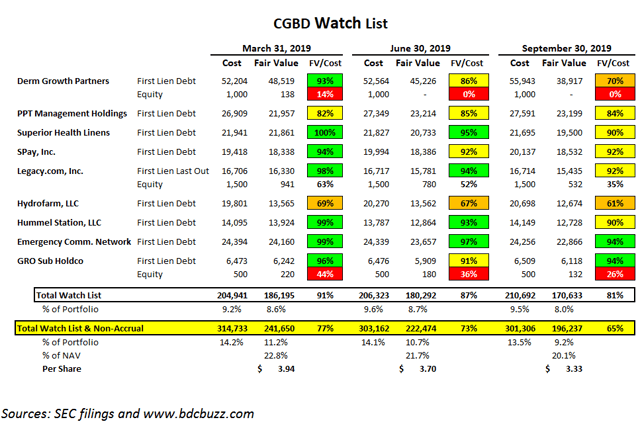

- CGBD reported Q3 2019 results on November 6, 2019, and I sold my position due to the additional declines of valuations in ‘watch list’ investments as shown below.

- Later this month, CGBD will likely report an additional investment on non-accrual which was previously considered its largest ‘watch list’ investment. Investors should be prepared for volatility.

TCG BDC (CGBD) is a business development company (“BDC”) externally managed by Carlyle GMS Investment Management and part of the Carlyle Group, which is a global alternative asset manager with $222 billion of AUM across ~360 investment vehicles providing CGBD access to scale, relationships and expertise, which has advantages including incremental fee income and higher investment yields.

On May 14, 2019, Michael A. Hart, CGBD’s Chairman of the Board and the Chief Executive Officer, informed the Board that he had determined to resign from the Board and as the Chief Executive Officer of the Company, effective December 31, 2019, to pursue other interests.

Linda Pace basically assumed the new role of President shortly after the announcement and formally took over on January 1, 2020. Overall, I see this as a positive for the company as she has added “more people, focus, and resources to the BDC platform”.

Previous Declines in CGBD’s Stock Price

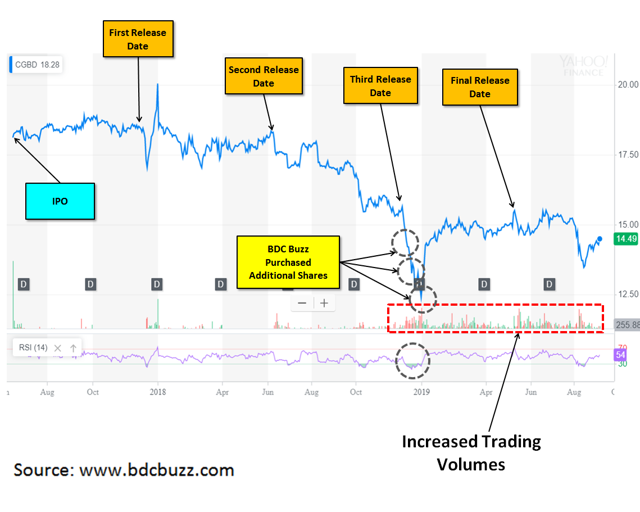

CGBD was formerly known as Carlyle GMS Finance, Inc. and closed its IPO on June 19, 2017, selling 9 million shares with four lockup periods each releasing 25% of an additional ~52 million pre-IPO shares. On April 24, 2019, the Board unanimously voted to accelerate the elimination of the final transfer restriction (the “Lock-Up”) applicable to shares purchased by investors prior to the company’s initial public offering (“Pre-IPO Shares”). The final “Release Date” resulted in additional technical pressure driving lower prices similar to previous Release Dates as shown below.

As discussed in previous articles, my last purchase of CGBD shares was during the December 2018 decline which was a combination that included the previous general market pullback as discussed by management on a previous call:

There is the release of the pre-IPO shares. As you probably also remember that puts enormous technical pressure on the stock. It had previously and history has shown that it did again here, but that’s also complemented or contributed with the overall sell-off in the BDC space as well as the overall general sell-off in the broader market.

BDC Buzz Sale of CGBD

As mentioned in each article, it is important for investors to closely watch the reported quarterly results for BDCs including potential credit issues that could result in lower net asset values (NAV/book values) as well as non-accruals that could result in lower dividend coverage. CGBD reported Q3 2019 results on November 6, 2019, and I sold my position at $14.25 due to the additional declines of valuations in ‘watch list’ investments as shown below:

Derm Growth Partners

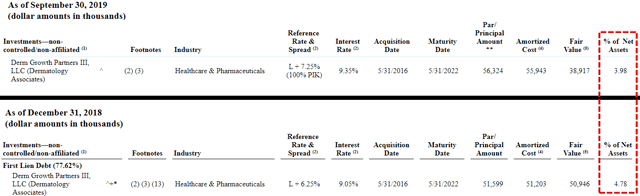

My last public article discussing CGBD was “Building A Retirement Portfolio With 6% To 9% Yield: Part 2” with an updated watch list for CGBD showing the recent declines including Derm Growth Partners at the top of the table (and largest). This investment has been continually marked down and as shown in the previous table, it was marked down to 70% of cost in Q3 2019.

Also, it was recently reported by Bloomberg that U.S. Dermatology Partners:

defaulted on a $377 million financing provided by a group of investment firms, according to people with knowledge of the matter. The dermatology practice owner is now reviewing its options, including a recapitalization or debt-for-equity swap with its current lenders, Golub Capital, The Carlyle Group Inc. and Ares Management, according to the people, who asked not to be identified because they aren’t authorized to speak about it.

Pieces of the loan, which matures in May 2022 and carries interest at 7.25% over Libor, are held in private credit vehicles called business development companies for Golub and Carlyle, according to regulatory filings. The BDCs were most recently marking the debt at about 69 cents to 74 cents on the dollar as of Sept. 30, the filings show.

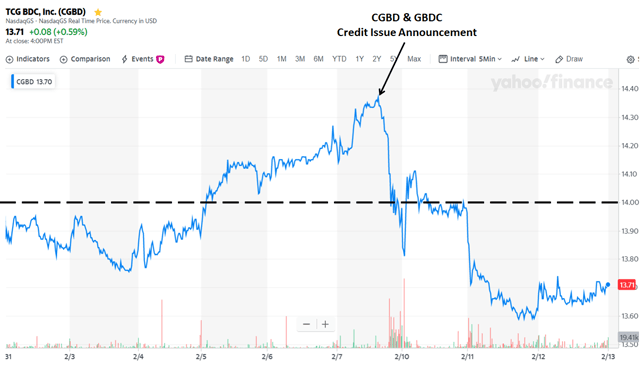

On February 7, 2020, I sent out multiple updates to subscribers mentioning “this could be a good time to sell some CGBD near recent highs” and ” I will hold my GBDC” due to the impact to the following loans:

- “Derm Growth Partners” for CGBD – $39 million FV or around $0.66/share = 4% maximum impact to NAV.

- “Oliver Street Dermatology Holdings, LLC” for GBDC – $23 million FV or around $0.17/share = 1% maximum impact to NAV.

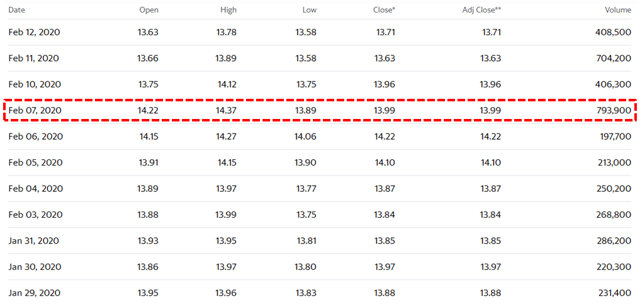

As shown below, volume picked up quite a bit on February 7, 2020, with most subscribers getting out higher or near $14.00.

As of September 30, 2019, Derm Growth Partners accounted for around 4% of CGBD’s NAV:

CGBD management discussed Derm Growth Partners on the previous call:

Q. “Okay, thank you. Could you also talk about, I think, Derm Growth Partners III, that’s something another one that you’re carrying, bit of a discount to costs. I’m not sure if there’s something incremental that happened this quarter or if you could just give an update on the company. Thank you.”

A. “Yeah, the update I’d give on that credit is we’re working through some operational and financial performance challenges with the sponsor and the company, but unlike some of the other positions such as dimensional which was the other large mark down this quarter. This is a first lien tranche, so we expect in the situation a very different outcome than we had on dimensional which obviously being junior debt, in a underperforming situation, the recovery prospects on that one is much difference, that’s an important distinction I would draw between the two borrowers.”

As mentioned in previous articles, management takes a conservative approach to valuing its portfolio:

When we held our initial earnings call as a public company back in August of 2017, I highlighted that based on our robust valuation policy, each quarter you may see changes in our valuations based on both underlying borrower performance as well as changes in market yields and that movement evaluations may not necessarily indicate any level of credit quality deterioration.

Source: CGBD Q4 2018 Earnings Conference Call Transcript

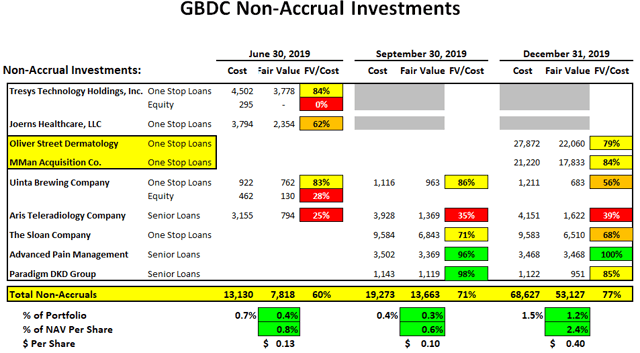

Golub Capital (GBDC) is also invested in this asset under the name Oliver Street Dermatology Holdings, LLC which was placed on non-accrual status during Q4 2019 as announced last week. During the most recent call, GBDC management discussed additional non-accruals (including Oliver Street Dermatology) mentioning that they are “cautiously optimistic that in respect of both companies, we are on a good path toward good recoveries”:

So non-accruals at cost and fair value increased in the most recent quarter to 1.6% and 1.3%, respectively. Whenever we think about non-accruals, we feel a degree of concern, right. We are naturally worriers. We worry about everything. One of the things we worry about is non-accruals. I want to make sure, though, that everyone keeps our concerns in appropriate context. So first, this quarter GBDC continued its strong track record of generating positive net realized and unrealized gains on investments. And that’s the metric that we think is, over time, the most important indicator of credit performance. That’s why we focus so much in our earnings presentation each quarter on the chart in our presentation depicting NAV per share over time. A second way we look at credit and overall credit quality is based on risk ratings, I think they show a great deal of stability quarter-over-quarter and for many quarters in a row. And the third contextual point I will make is that the latest figures indicate that even with this small increase, we are still in the low end of the range of the industry and we are in our historical range in respect of non-accruals at cost. So I don’t want to make any of this sound like it’s more dramatic than it is. With that said, we are working hard with the managements of the two companies that we put on non-accrual this quarter and I can’t get into the details of either of the two situations, but what I can say is, I am cautiously optimistic that in respect of both companies, we are on a good path toward good recoveries.

Source: GBDC Q1 2020 Results – Earnings Call Transcript

GBDC’s investment in Oliver Street Dermatology was marked at 79% of cost which is above CGBD’s 9/30 valuation at 70% implying that this asset was conservatively marked even before CGBD adds to non-accrual. This is a sign of quality management which is why I will be closely watching upcoming results for CGBD.

CGBD Share Repurchases, Management & Fee Agreement

I consider CGBD to have higher quality management for various reasons including the previously discussed conservative asset valuations, share repurchases, previously waived management fees, conservative dividend policy driving continued/potentially additional special dividends and a shareholder friendly-fee structure of 1.50% base management fee (compared to 2.00%) and an incentive fee of 17.5% (compared to the standard 20.0%). However, the current fee agreement is not best-of-breed as it does not include a ‘total return hurdle’ to take into account capital losses when calculating the income incentive fees.

On November 4, 2019, the Board authorized a 12-month extension of its $100 million stock repurchase program at prices below reported NAV per share through November 5, 2020, and in accordance with the guidelines specified in Rule 10b-18 of the Exchange Act. The company has repurchased around $52 million worth of shares representing approximately $0.14 in NAV accretion for shareholders.

We continue to be active in share repurchases during the third quarter as we do not believe our valuation reflects the intrinsic value of our company with a broad capabilities of the Carlyle platform. We repurchased $17 million of shares during the quarter and inception to-date, the $52 million in repurchase activity has led to $0.14 in accretion to NAV. We have approximately $48 million remaining on our $100 million repurchase authorization which earlier this week, our board extended for another year. It is our intent to continue repurchasing shares at or near our current valuation.”

Source: CGBD Q3 2019 Results – Earnings Call Transcript

Conclusion and CGBD Recommendations

- If you are like me, a conservative investor that does not like surprises, you likely already sold CGBD. Those that have not should be ready for volatility over the next two weeks.

- If you are a more aggressive investor looking for higher returns and yield, you may have been buying including when the stock was trading at $13.15 (20%+ discount to NAV of $16.58) waiting for the company to report positive results and NAV reflation.

Items to keep in mind:

- On January 1, 2020, Linda Pace formally took over as CEO. Overall, I see this as a positive for the company as she has “added more people, focus, and resources to the BDC platform”.

- Previously, CGBD repurchased around $52 million worth of shares and hopefully continued to repurchase shares in Q4 2019 that will have a positive impact to NAV.

- CGBD takes a conservative approach to valuing its portfolio assets.

- CGBD had already marked Derm Growth Partners at 70% of cost as of September 30 compared to GBDC that marked it down to 79% of cost as of December 31.

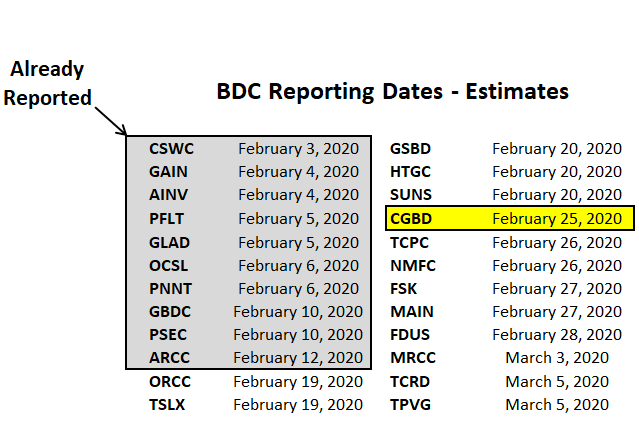

My best guess is that CGBD’s stock price will drop after the company reports Q4 2019 results on February 25, 2020 (see table below) due to continued overreaction as this is a relatively new public company and has already reported a few quarters with credit issues.

What will I be doing?

I will be doing the same thing that I mentioned in the CGBD Deep Dive from November 2019:

I will not be repurchasing shares until after the company reports Q4 2019 results.

This information was previously made available to subscribers of Premium BDC Reports, along with:

- CGBD target prices and buying points

- CGBD risk profile, potential credit issues, and overall rankings

- CGBD dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

BDCs have started to report calendar year-end results. Investors should be watching for potential portfolio credit issues that could lead to credit rating downgrades. Lower ratings would likely drive higher borrowing expenses that could put downward pressure on net interest margins and dividend coverage over the coming quarters.

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.