The following is from the ARCC Update that was previously provided to subscribers of Premium BDC Reports along with revised target prices, dividend coverage and risk profile rankings, potential credit issues, earnings/dividend projections, quality of management, fee agreements, and my personal positions for all business development companies (“BDCs”).

Quick Update:

Last month, there was a notice of “3,000 more layoffs are expected in New Jersey as health care industry changes and store closings are expected to impact the state” that included Alcami Corporation which is expected to layoff 27 people on December 27, 2019. It should be noted that this investment is already included in Ares Capital (ARCC) ‘watch list’ and will be discussed in the updated Deep Dive report.

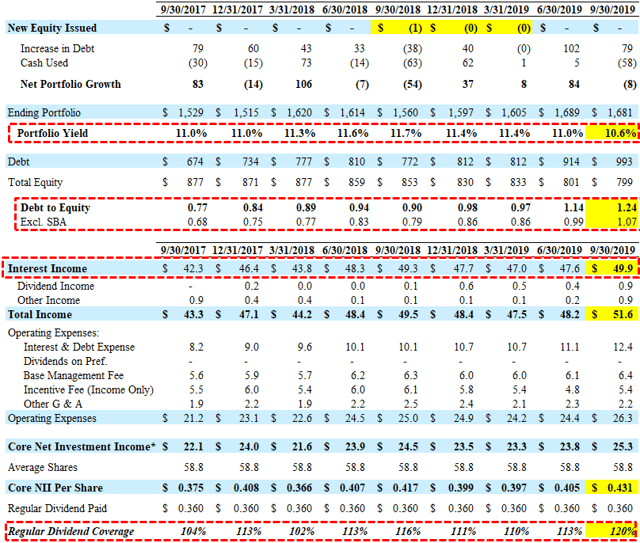

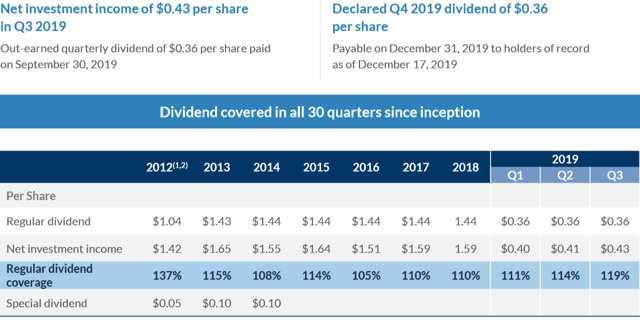

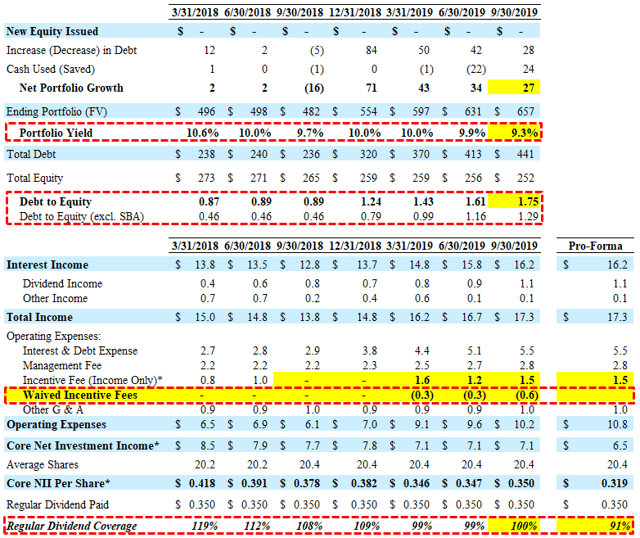

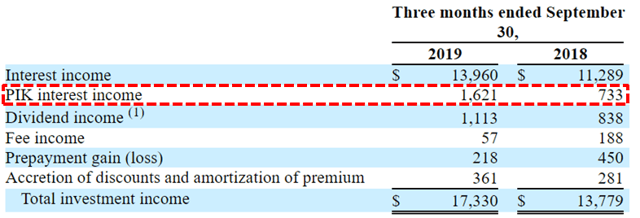

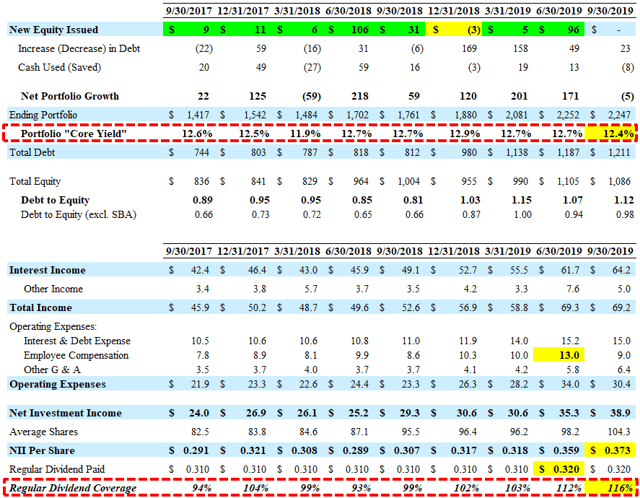

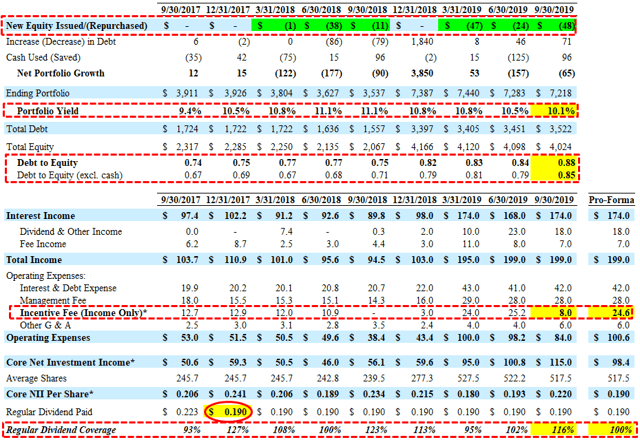

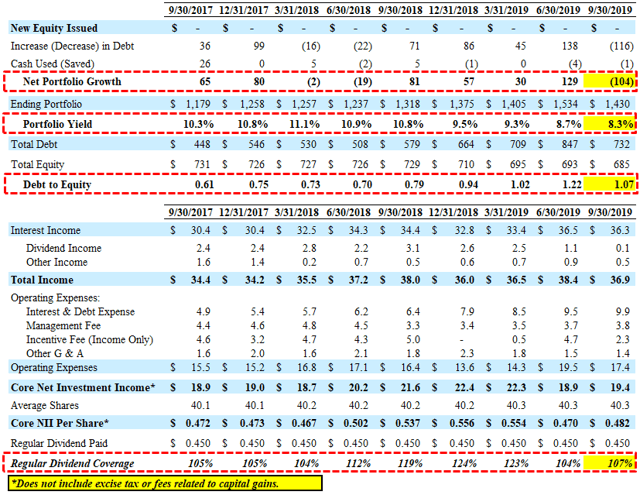

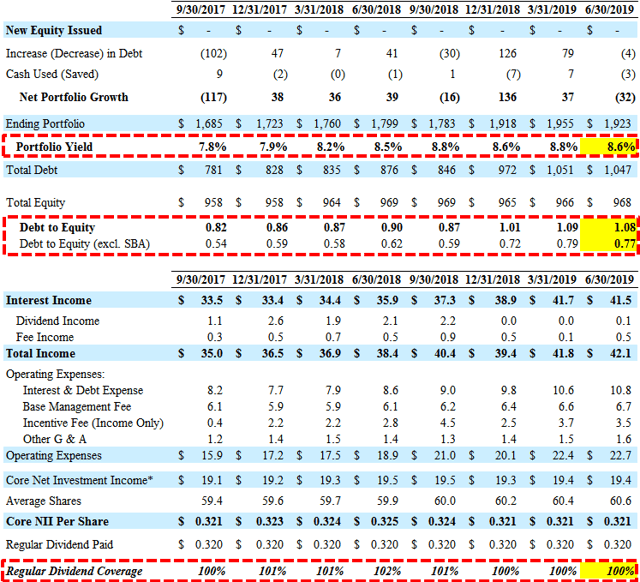

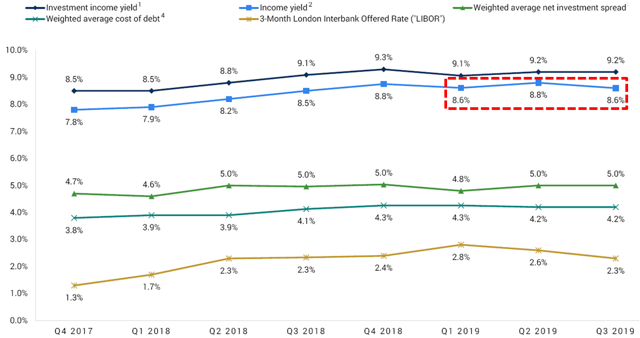

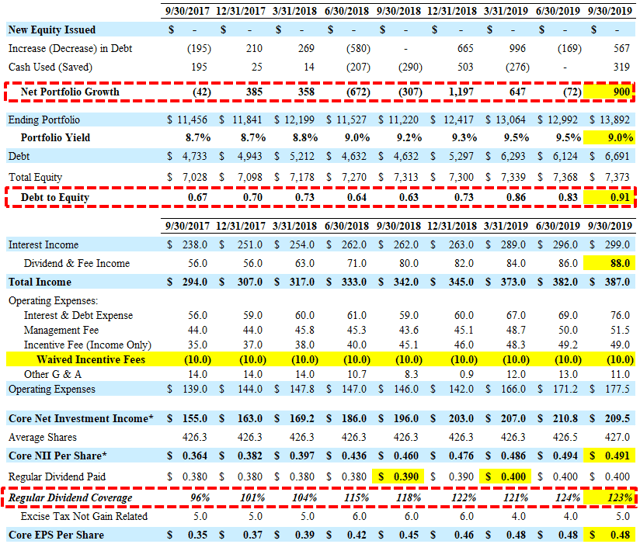

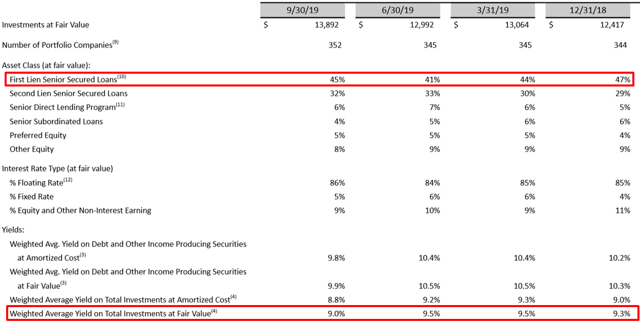

Ares Capital (ARCC) beat its base-case Q3 2019 projections mostly due to higher-than-expected portfolio growth and continued higher dividend and fee income covering its regular dividend by 123%. Its portfolio yield declined more than expected (from 9.5% to 9.0%) due to onboarding investments at lower yields. The company declared a fourth quarter dividend of $0.40 per share and confirmed the additional dividend of $0.02 per share per quarter.

Kipp deVeer, CEO: “We reported another strong quarter of core earnings well in excess of our dividend and experienced continued stable credit quality. We continue to benefit from our broad market coverage and extensive relationships which enable us to originate attractive investments and remain highly selective.”

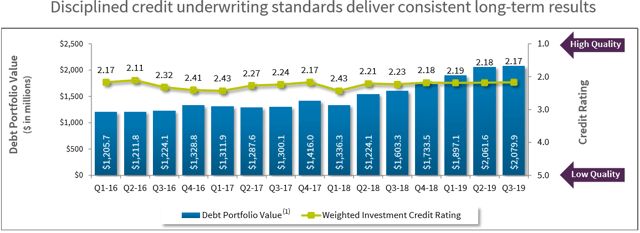

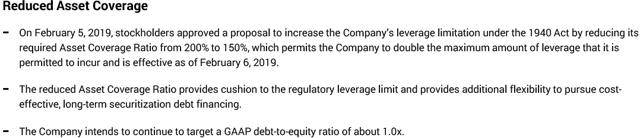

Its debt-to-equity reached its highest level increasing from 0.83 to 0.91 As mentioned in previous reports, ARCC expects to use incremental leverage to continue to invest “primarily in its current mix of investments with no fundamental change in its investment objective and intends to target a debt to equity range of 0.90x to 1.25x.” Effective June 21, 2019, Ares Capital’s asset coverage requirement applicable to senior securities was reduced from 200% to 150% and its annual base management fee was reduced from 1.5% to 1.0% on all assets financed using leverage over 1.0x debt to equity.

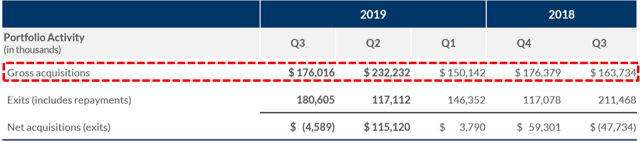

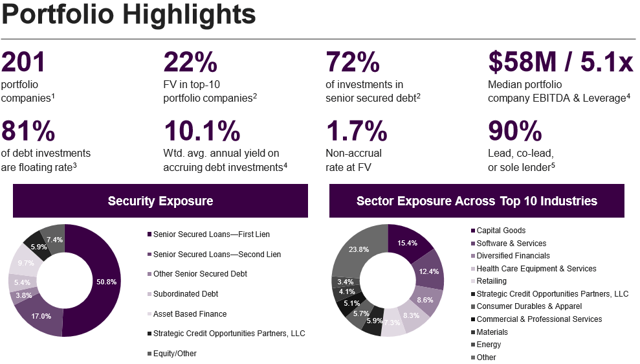

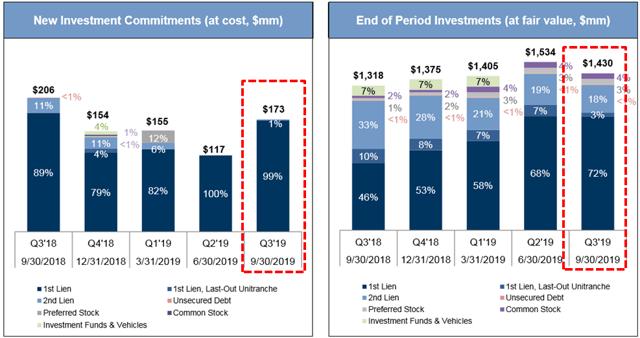

During Q3 2019, ARCC made $2.4 billion in new investment commitments, 90% were in first lien senior secured loans, 7% were in second lien senior secured loans, 1% were in the subordinated certificates of the Senior Direct Lending Program (“SDLP”), and 2% were in other equity securities. Also, the company exited $1.4 billion of investment commitments, 73% were first lien senior secured loans, 9% were second lien senior secured loans, 10% were senior subordinated loans, 7% were subordinated certificates of the SDLP, and 1% were other equity securities.

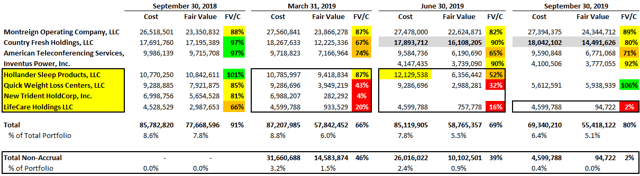

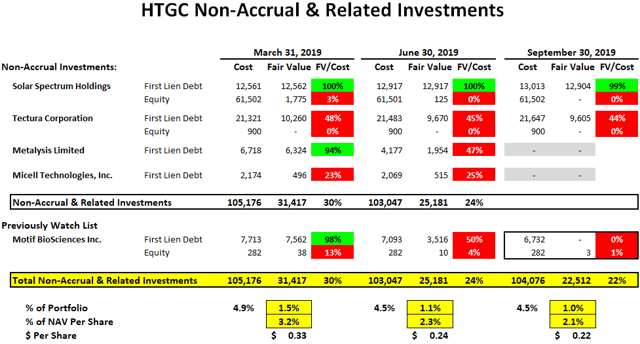

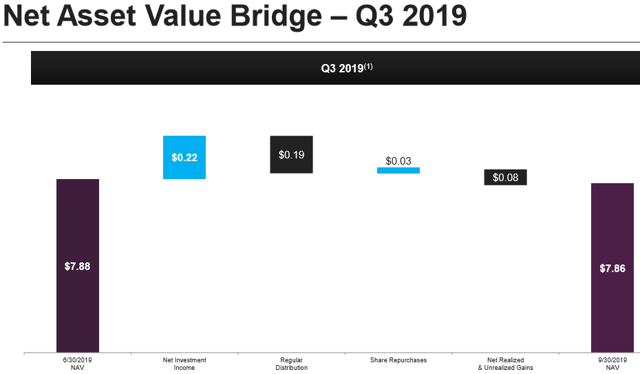

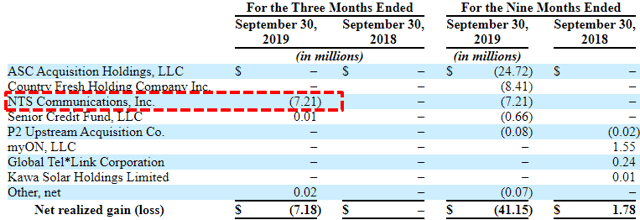

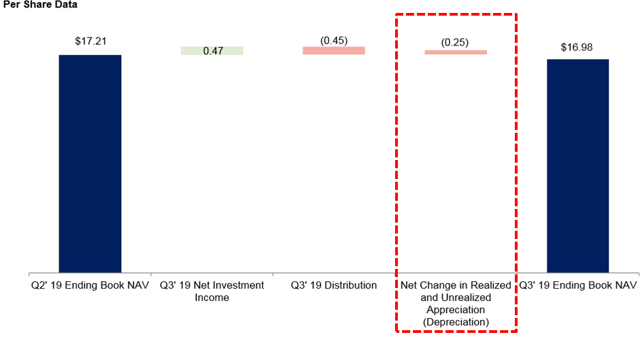

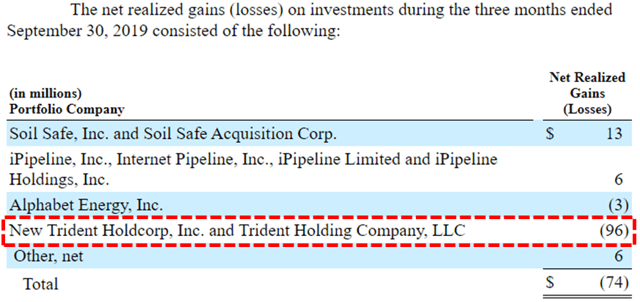

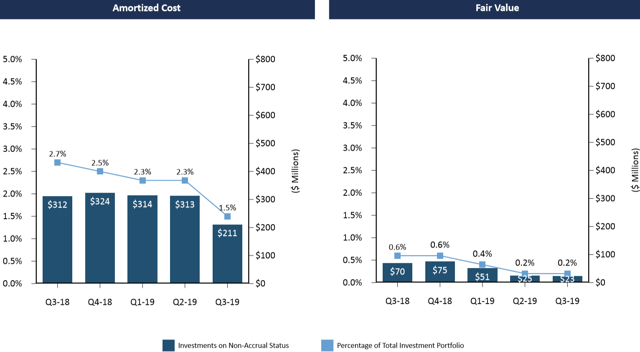

Its net asset value (“NAV”) per share remained mostly stable (decreased from $17.27 to $17.26) due to net unrealized/realized losses during the quarter mostly offset by overearning the dividends. ARCC experienced net realized losses of $63 million during Q3 2019 due to exiting its investment in New Trident Holdcorp that was previous its largest non-accrual investment:

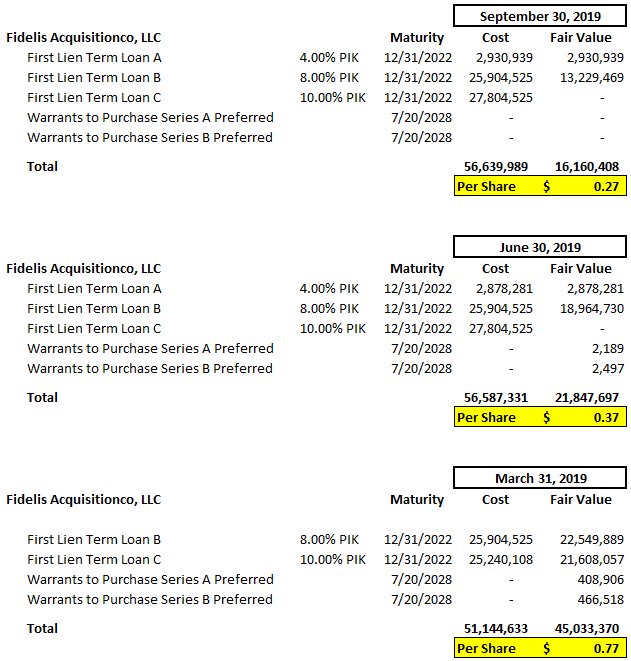

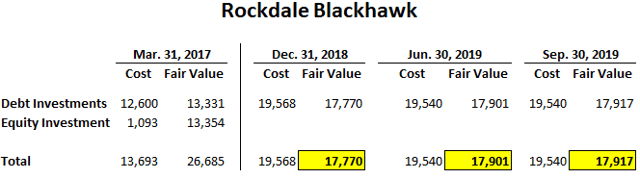

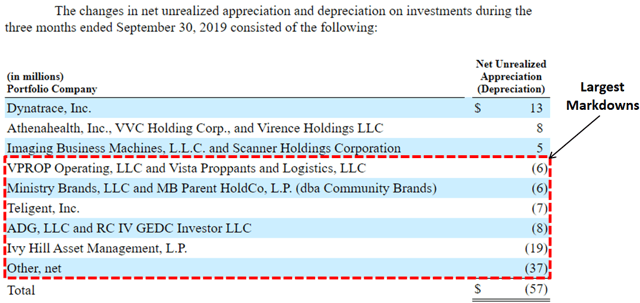

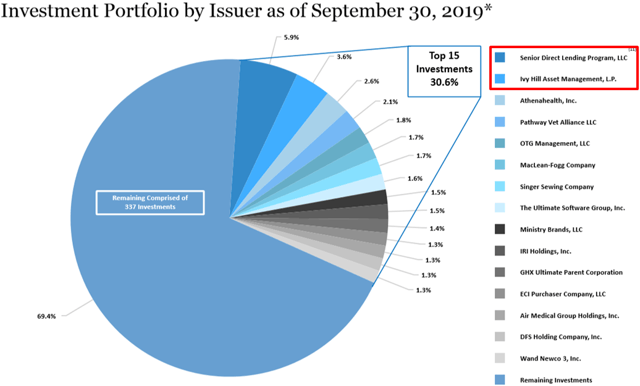

Some of the largest markdowns during Q3 2019 were Ivy Hill Asset Management (same as the previous quarter), and watch list investment ADG, LLC and RC IV GEDC.

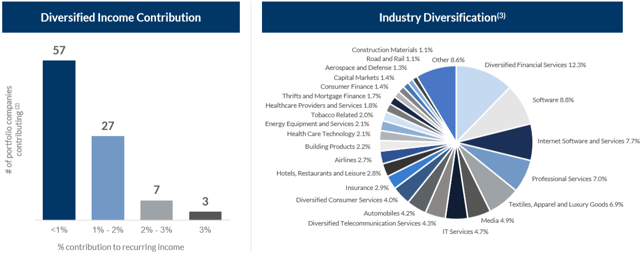

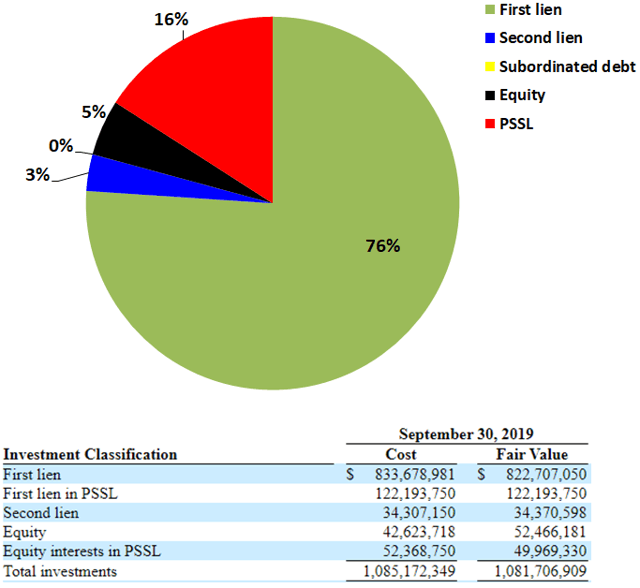

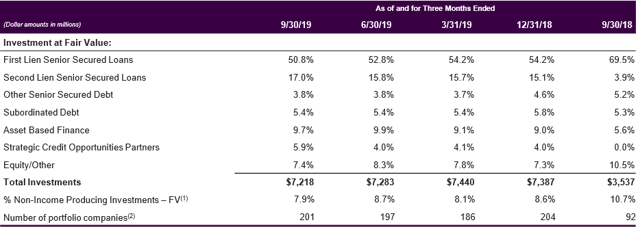

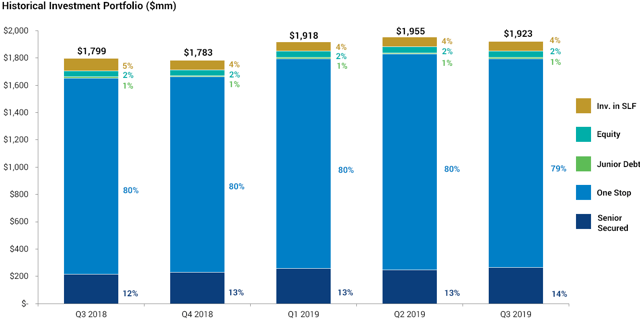

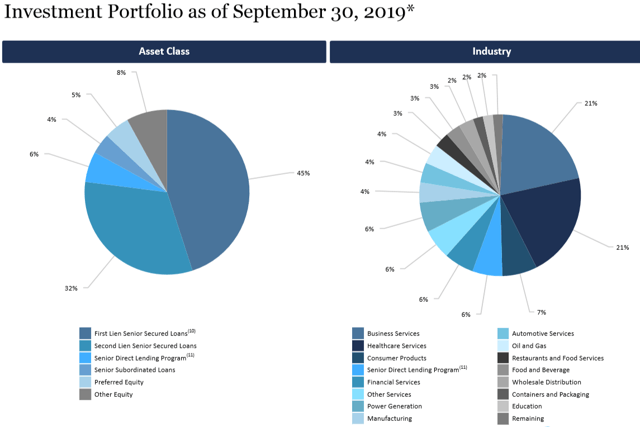

There was a positive shift in its portfolio asset mix toward first-lien positions that now account for 45% of the portfolio (previously 41%) along with 32% second-lien, 6% of subordinated certificates of the SDLP, 4% of senior subordinated loans, 5% of preferred equity securities and 8% of other equity securities.

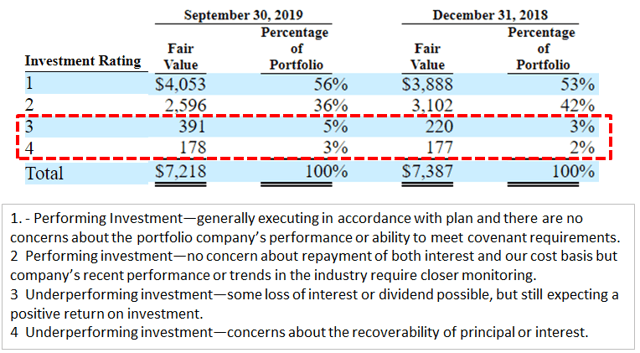

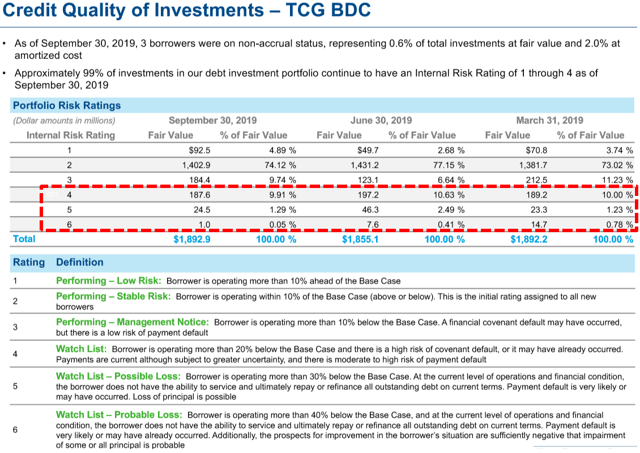

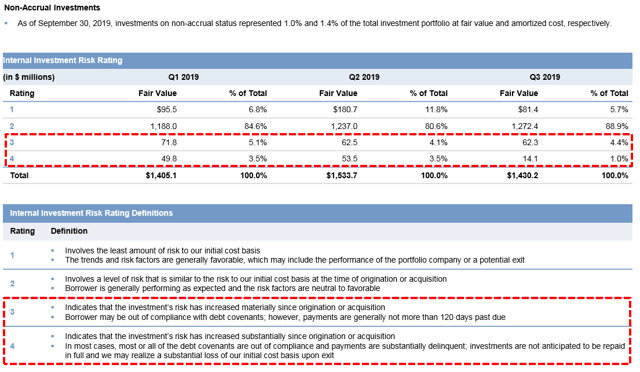

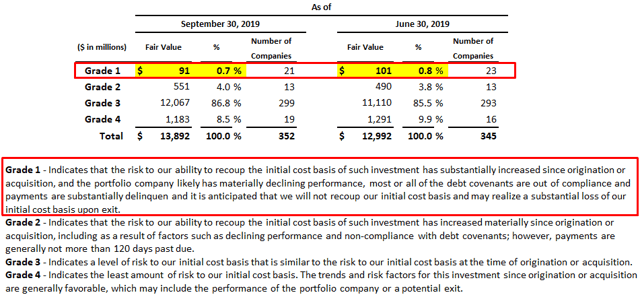

Non-accrual investments declined due to exiting New Trident Holdcorp and remain low at 0.2% fair value and 1.5% of cost with the weighted average grade of the investments in the portfolio at fair value remains around 3.0.

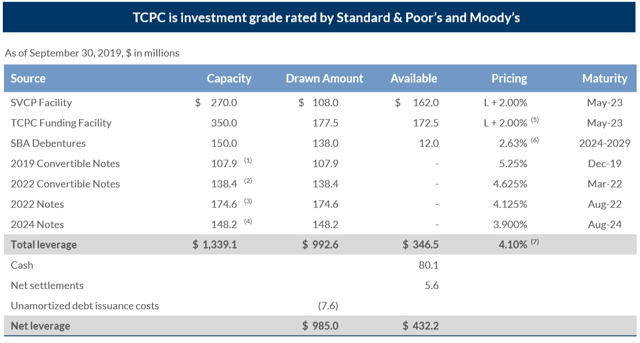

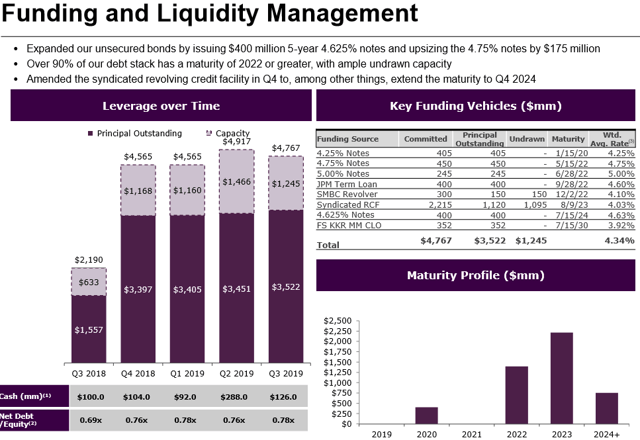

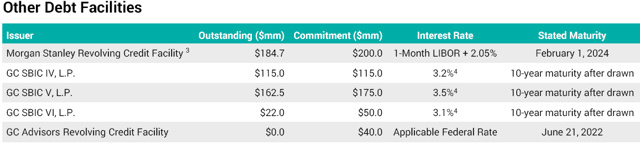

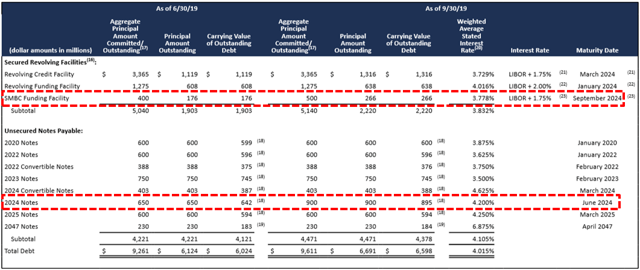

As of September 30, 2019, ARCC had $253 million in cash and cash equivalents and approximately $2.9 billion available for additional borrowings under its existing credit facilities.

- In September 2019, ARCC issued an additional $250 million in aggregate principal amount of unsecured notes, which bear interest at a rate of 4.200% per year and mature on June 10, 2024 (the “Additional 2024 Notes”). The Additional 2024 Notes were issued at a premium to the principal amount.

- In September 2019, ARCC amended the SMBC Funding Facility to, among other things, increase the commitments under the facility from $400 million to $500 million, with the ability to upsize to $800 million.

Penni Roll, CFO: “In the third quarter, we further executed on our strategy of increasing and extending our sources of committed financing. After upsizing and extending the maturity of our SMBC Funding Facility, as well as successfully re-opening our 2024 notes, we ended the quarter with nearly $3 billion of available cash and undrawn committed borrowing capacity. We believe our deep liquidity position and long dated funding enhances the strength of our balance sheet and supports our ability to invest opportunistically across varying market conditions.”

—————–

—————–

In February 2019, ARCC’s Board authorized an amendment to its stock repurchase program to increase the program from $300 million to $500 million and extend the expiration date of the program from February 28, 2019 to February 28, 2020. There were no shares repurchased during the three months ended September 30, 2019. As of September 30, 2019, the approximate dollar value of shares that may yet be purchased under the program was $493 million.

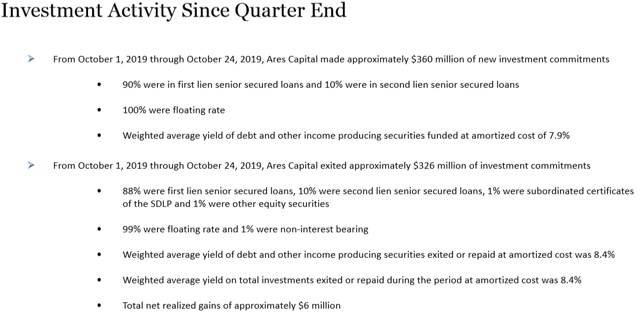

From October 1, 2019 through October 24, 2019, ARCC made new investment commitments of approximately $360 million, of which $311 million were funded. Of these new commitments, 90% were in first lien senior secured loans and 10% were in second lien senior secured loans. The weighted average yield of debt and other income producing securities funded during the period at amortized cost was 7.9%.

From October 1, 2019 through October 24, 2019, ARCC exited approximately $326 million of investment commitments. Of the total investment commitments, 88% were first lien senior secured loans, 10% were second lien senior secured loans, 1% were subordinated certificates of the SDLP and 1% were other equity securities. The weighted average yield of debt and other income producing securities exited or repaid during the period at amortized cost was 8.4% and the weighted average yield on total investments exited or repaid during the period at amortized cost was 8.4%. On the approximately $326 million of investment commitments exited from October 1, 2019 through October 24, 2019, ARCC recognized total net realized gains of approximately $6 million.

In addition, as of October 24, 2019, Ares Capital had an investment backlog and pipeline of approximately $665 million and $265 million, respectively.

—————–

As mentioned in previous reports, dividend coverage should continue to improve (excluding the fee waivers that end in Q3 2019) over the coming quarters due to the following:

- Utilizing its 30% non-qualified bucket for higher portfolio yield and fee income. This includes the ramping of its SDLP joint venture and Ivy Hill Asset Management.

- Increased leverage and portfolio growth

- Increased fee income

- Reduced borrowing rates

BDCs are allowed a maximum of 30% of total assets to be considered non-qualified which includes the Senior Direct Lending Program (“SDLP”) and Ivy Hill Asset Management (“IHAM”). ARCC continues to utilize its 30% non-qualified bucket which includes the SDLP and IHAM that currently account for almost 10% of the portfolio.

—————–

This information was previously made available to subscribers of Premium BDC Reports, along with:

- ARCC target prices and buying points

- ARCC risk profile, potential credit issues, and overall rankings

- ARCC dividend coverage projections and worst-case scenarios

- Real-time changes to my personal portfolio

To be a successful BDC investor:

- As companies report results, closely monitor dividend coverage potential and portfolio credit quality.

- Identify BDCs that fit your risk profile.

- Establish appropriate price targets based on relative risk and returns (mostly from regular and potential special dividends).

- Diversify your BDC portfolio with at least five companies. There are around 50 publicly traded BDCs; please be selective.